Mortgage Rates Tick Back Up as Iran War Stokes Inflation Fears

Share News:

A lot of hopes have been pinned on mortgage rates going down this year, but it seems this new war with Iran is poised to be a check on additional benchmark interest rate cuts and an overall drag on housing market activity.

“Economic uncertainty is not a position from which many people are interested in making the largest purchase of their life, and the conflict in Iran just added to the anxiety pile that already included tariffs, last year’s soft labor market, stock market volatility, and AI job loss concerns,” said Realtor.com senior economist Joel Berner.

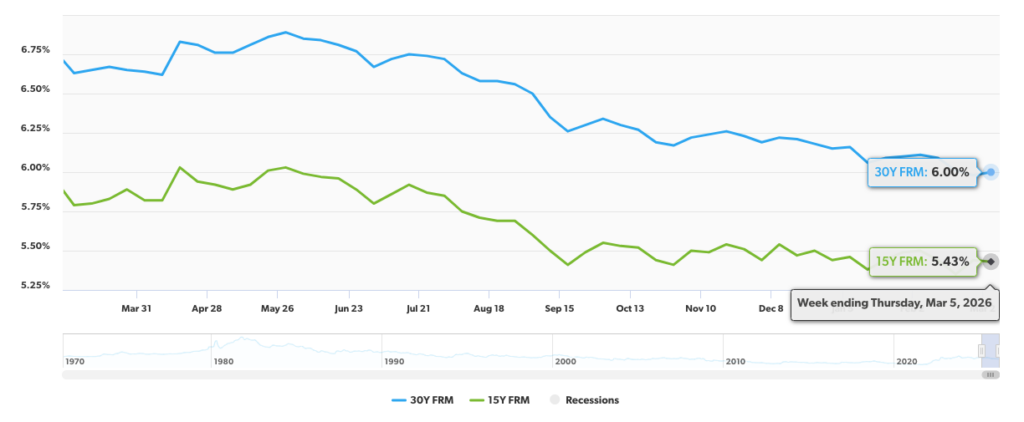

Late last month, Freddie Mac put the average 30-year mortgage rate at 5.98%, below the 6% line that has been bandied about by market observers as a significant psychological threshold that could activate more prospective buyers. Just this week, though, the 30-year ticked back up to 6%.

Berner said that the war in Iran is stoking fears of resurgent inflation. Those fears are not unfounded considering the implications for the price of oil, which skyrocketed following the conflict’s outbreak. The price of oil is an input in the production and distribution of goods all over the world, afterall, so it’s something many Americans could feel the longer the war goes on — and not just at the gas pump.

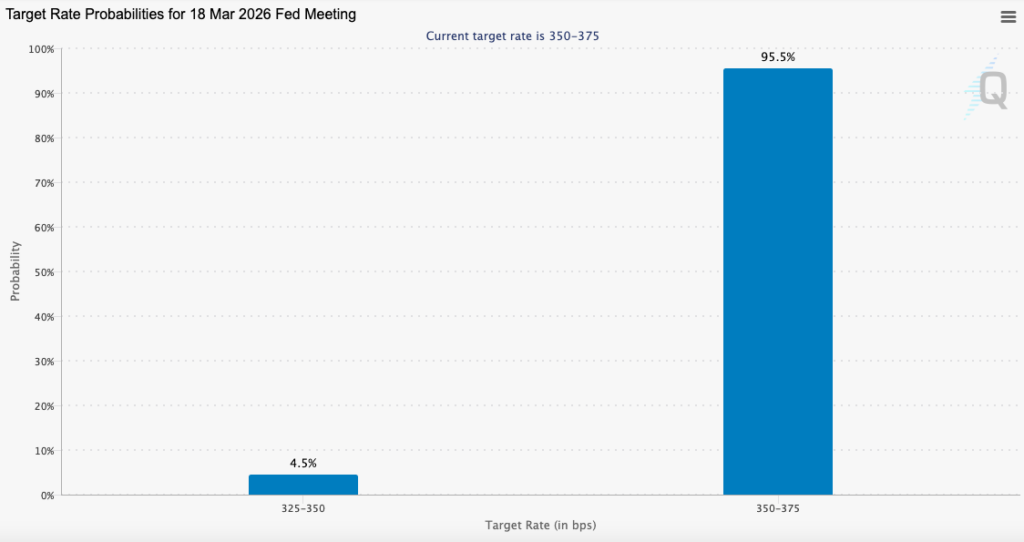

The Federal Reserve will also be less likely to pursue benchmark interest rate cuts across the year if inflation rebounds. While few were betting on a cut at the central bank’s upcoming policy setting meeting on March 18 before the war started, the FedWatch tool is now projecting a 95.5% chance the Fed stands pat.

Mortgage rates aren’t directly tied to the Fed’s benchmark interest rate, but they do tend to follow the benchmark’s trajectory based on investor behavior, which is informed by the central bank’s read of the economy.

John Williams, president of the New York Federal Reserve, told Yahoo! Finance that the war would “obviously” have an impact on the nearer-term inflation outlook.

“We’ll have to see how persistent this is and how long this is, but it would have an effect on overall inflation… Nobody can be sure of how long this will last or the broader implications of these events in terms of financial conditions and oil prices,” he said.

Federal Reserve rate policy, however, typically focuses on longer-term outlooks based on core inflation, which excludes oil and energy prices. So, the jury’s still out.

Prior to the outbreak of war, the housing market was starting to look a little friendlier to buyers, with increased inventory and mortgage rates down significantly from the post-COVID high of 7.79%. Maybe more importantly, sellers are starting to come back down to Earth after enjoying rising valuations over quite some time, with more homes selling under asking price.

“The sellers are still stuck on the glory days of a few years ago when their home values seemed to skyrocket,” said Mike McWethy, executive vice president of Texans Credit Union in Richardson. “When they try to sell their home, they have to negotiate downwards. We’re seeing that a lot.”

We spoke with McWethy around the time the 30-year mortgage dipped below the 6% threshold.

Many existing homeowners remain reluctant to sell, though, because they are locked into mortgage rates near 3%, which is keeping some inventory off the market in the D-FW. Homes priced under about $500,000 are still moving at a relatively healthy pace amid continued population growth in North Texas, McWethy said, while larger and more expensive properties are seeing less activity.

“If you’re in a very large home and you’re sitting on a 3% mortgage rate, well, those homes are not moving unless there’s a forced situation,” he said.

Lawrence Yun, chief economist for the National Association of Realtors, previously said several million prospective homebuyers would be able to enter the market if rates got below 6%. We might have to wait a little while longer now to see if that pans out because of the war. While mortgage rates around 6% are historically normal, many buyers still perceive them as high after a decade of low borrowing costs. Rising property taxes and homeowners insurance are adding to the situation, often producing sticker shock for first-time buyers once they see the full monthly payment.

“We’re just having to come to terms with getting to a normal, correct environment,” McWethy said. “For those that are sitting in a good place financially and are able to act, it’s a great time to buy with housing prices having to come down [after appraisal].”