Lower Mortgage Rates, Higher Stakes for the Federal Reserve

Share News:

It has been a whirlwind of news on the mortgage rates front over the last few days as the 30-year note crossed a critical threshold. Meanwhile, the independence of Federal Reserve policy appears more under threat than ever amid a criminal investigation into the central bank’s chair.

First, Mortgage Rates

Last Thursday, President Donald Trump said he was directing Fannie Mae and Freddie Mac, both still under federal conservatorship, to purchase $200 billion in mortgage bonds. The following day, mortgage rates continued their downward trajectory and ticked just below 6% for the first time in more than three years.

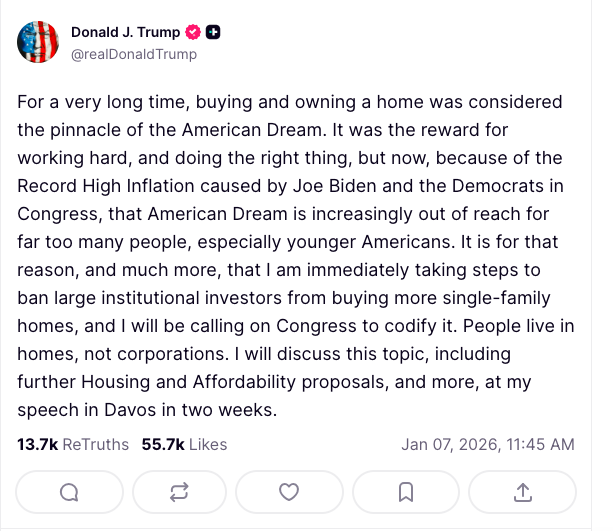

On Monday, the White House claimed the dip could be attributed to the president’s pronouncements on the housing front. In addition to the mortgage bond directive, Trump had also said he was going to take steps to ban institutional investors from buying up single-family housing stock.

There’s been a lot of clamoring about high mortgage rates sidelining a lot of would-be homebuyers. While this refrain tends to ignore the sky-high home valuations, rates have been more than double the 2-3% lows seen in the aftermath of the COVID-19 pandemic, making monthly payments a serious challenge for many.

Lawrence Yun, chief economist of the National Association of Realtors, previously said some 5.5 million more American households would be able to afford to buy a home if the 30-year hit 6% or lower.

No doubt the recent dip below 6% is welcome news to prospective buyers and real estate agents, but some industry experts are hesitant to put much stock in Trump’s mortgage bond play, claiming any impact would be short-lived if felt at all.

Realtor.com senior economist Joel Berner, for instance, said it was “unlikely to meaningfully alter long-term mortgage pricing.” Other experts similarly told the outlet that activity in the mortgage-backed securities market has basically already been priced into rates.

Still, every little bit helps, and NAR has been advocating for such a move. The association’s executive vice president, Shannon McGahn, said Trump’s $200 billion purchase “reflects the kind of market-stabilizing policy we’ve championed. We stand ready to work with the administration to ensure it delivers real relief for homebuyers and the broader housing market.”

According to NBC News, analysts at the investment bank UBS said in a client note that Trump’s move could result in the 30-year creeping down another 0.2%, writing, “This decline may provide a boost to both new construction demand and existing home turnover.”

Short-Term Gains at the Expense of Long-Term Credibility?

Now, mortgage rates aren’t directly tied to the Federal Reserve’s benchmark interest rate, but they do tend to run in tandem. The Fed influences mortgage rates by shaping economic expectations. When the central bank raises or lowers its benchmark rate, it signals how it views inflation and the broader economy. Higher rates often push Treasury yields up as investors anticipate tighter monetary policy, which in turn leads to higher mortgage rates. On the flip side, when the Fed cuts rates to stimulate growth, yields often fall and mortgages go down with them.

This whole dynamic, however, is supposed to be predicated on the independence of the Federal Reserve, an institution ostensibly run by impartial economists and financial experts.

Enter President Donald Trump.

It’s no secret the president has been incredibly active in the economy. His tariff-fueled trade policy has caused plenty of anxiety in the housing market over the last year, and he’s been vocal about his desire for the Fed to issue bigger and more frequent interest rate cuts.

Being vocal is putting it mildly. Trump has been publicly beating up on Fed Chair Jerome Powell and the majority of policy-setters on the Fed board, blaming them for holding back the economy. Things have escalated considerably, though.

On Friday, the Department of Justice issued grand jury subpoenas to the Federal Reserve. Prosecutors are examining whether Powell gave false or misleading testimony to the Senate Banking Committee last year when he discussed the roughly $2.5 billion overhaul of the central bank’s offices in Washington, D.C. The project has drawn criticism for cost overruns and management issues.

Critics of the probe — which include former Fed chairs, economists, and some lawmakers from both parties — argue it risks politicizing the Federal Reserve and undermining confidence in U.S. monetary policy.

“The threat of criminal charges is a consequence of the Federal Reserve setting interest rates based on our best assessment of what will serve the public, rather than following the preferences of the President,” Powell said in a statement over the weekend. “This is about whether the Fed will be able to continue to set interest rates based on evidence and economic conditions — or whether instead monetary policy will be directed by political pressure or intimidation.”

It’s never a dull moment on the mortgage front.