Is Dallas-Fort Worth Real Estate Overvalued? And is The Market Headed For a Correction?

Share News:

The housing market is like a Las Vegas card game these days. Should you tell the dealer to hit? Should you hold? Surely, with home prices where they are in the Dallas-Fort Worth region, it feels like a gamble to purchase real estate right now.

And that might not be far from the truth.

A new report using data from The Real Estate Initiative at Florida Atlantic University shows that many major metropolitan areas in the nation are at or above the valuation levels recorded before the housing bubble burst in 2008. While that catastrophic collapse was caused by fast-and-loose lending, the situation we face now is much different.

According to Fortune:

At the latest reading in March, Florida Atlantic University researchers found every one of America’s 100 largest housing markets overpriced relative to what economic fundamentals in the market would support. That includes 44 markets overpriced by at least 30% and 13 overpriced by at least 50%.

The most overpriced markets are Boise (by 75%); Austin (66%); Ogden, Utah (63%); Las Vegas (60%); and Atlanta (60%). Those places have all seen an influx of new residents amid the pandemic’s “work from anywhere” boom. That, in part, explains why home prices there have soared well above what local incomes can afford. It also raises the question: If a 2023 recession does come and employers finally have the economic power to force staffers back into the office, will those housing markets be at a higher risk of home price correction?

What could force a correction in the housing market? Skyrocketing interest rates, for starters. And those same interest rates are causing some sellers to drop their prices already. That’s what new data from Redfin shows:

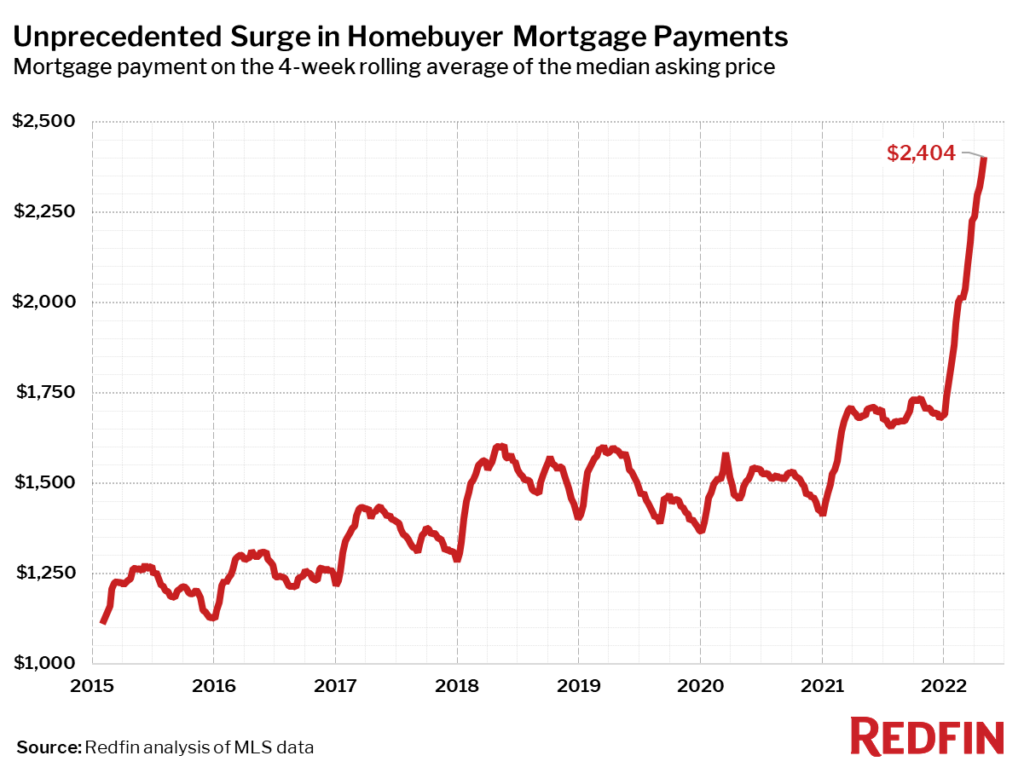

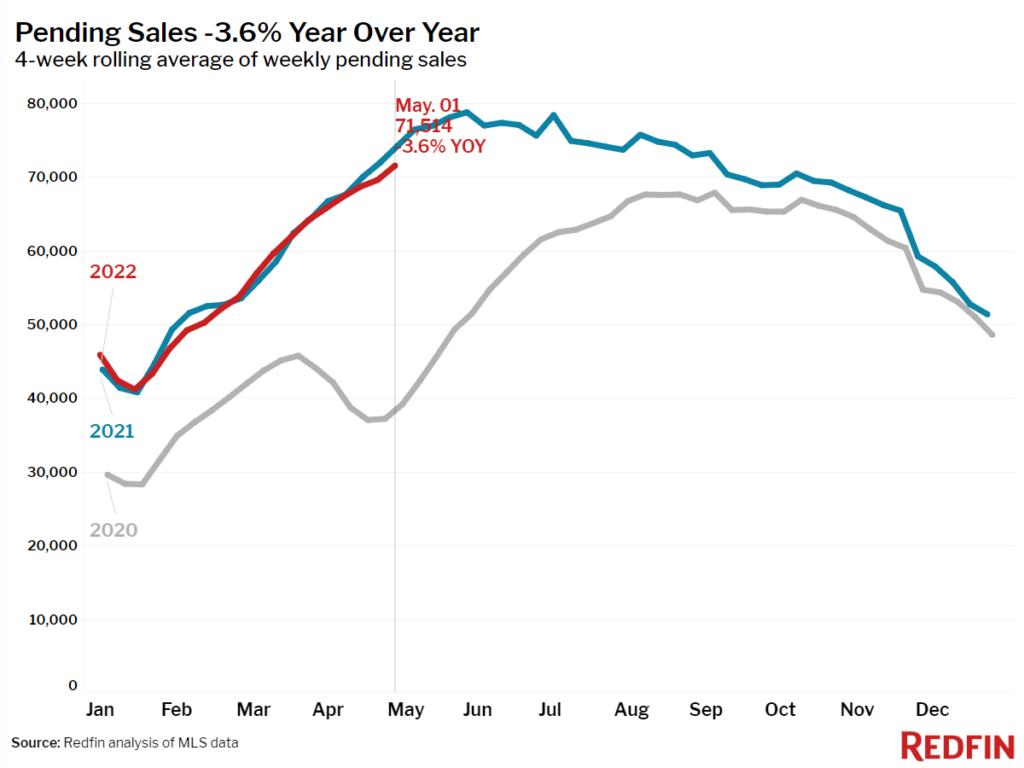

The share of home sellers who dropped their asking price shot up to a six-month-high of 15% for the four weeks ending May 1, up from 9% a year earlier. The 5.9% increase is the largest annual gain on record in Redfin’s weekly housing data back through 2015. For homebuyers, the typical monthly mortgage payment skyrocketed a record 42% to a new high during the same period. Although a growing share of sellers are responding to the palpable drop in homebuyer demand by lowering their prices, sellers remain far outnumbered by buyers, so the typical home flies off the market at the fastest pace on record and for more than its asking price.

“Homebuyers continue to be squeezed in nearly every way possible, which is causing some to take a step back from the market,” said Redfin chief economist Daryl Fairweather. “Unfortunately for buyers hoping to find a deal as competition cools, sellers are pulling back even faster, which is keeping the market deep in seller’s territory. So even though price drops are becoming more common, most homes are still selling above asking price and in record time.”

Florida Atlantic University’s numbers for the Dallas-Fort Worth-Arlington MSA show that as of March, our region’s market could be overvalued by 45.85 percent. In March of 2020, the data showed our MSA as being overvalued by 9.66 percent. In 2007, right before the housing market collapsed, Florida Atlantic University’s data said that our MSA was overvalued by 2.79 percent.

It’s no surprise for buyers agents that homes in the Dallas-Fort Worth region are, as Florida Atlantic University researchers called it, “overvalued.” And with Redfin‘s data showing price reductions for some homes, that has to be welcome news. But is every price reduction the result of higher interest rates and decreasing buying power from those in the market for a home?

“We’re seeing the results of buyer exhaustion. These poor guys and gals are no longer willing to be one of 40 offers and pay so far beyond an already inflated asking price,” said Travis Lee-Moore with Coldwell Banker in Fort Worth. “The sellers got greedy for a minute and their agents were actually encouraging them to do so. Nobody can afford to or wants to wait several years for their purchase price to catch up to their actual value and defer their equity like that. It never was sustainable and I’m surprised it lasted as long as it did.”

Of course, real estate is a local business, and not all areas are the same. While prices are coming down in some areas, other neighborhoods and towns are holding strong.

“With interest rates on the rise, monthly mortgage costs are increasing. However, I have not seen a slow down in the number of clients that are still eagerly looking to purchase a home,” said Katrina Whatley, an Oak Cliff Realtor with Ultima Real Estate. “Multiple offers above the asking price are still the norm. Rising interest rates have not deterred buyers in this market.”

So, we find ourselves asking again: Are we in for a market correction? Is this a bubble that is going to burst?

Not so much according to Mark Zandi, chief economist at Moody’s Analytics, in the Fortune report:

Mark Zandi, chief economist at Moody’s Analytics, doesn’t foresee a housing bust over the coming year. However, he says “overvalued” housing markets could see home prices fall 5% to 10% over the next 12 months while national home price growth flatlines to zero. Why? The economic shock caused by spiking mortgage rates this year, he says, should finally rein in the rate of home price growth. We’re already seeing signs of a cooling housing market.

While Moody’s Analytics own research finds 96% of housing markets are overvalued, Zandi won’t call this a housing bubble. In order for it to be a housing bubble, it would need both home price overvaluation and speculation in the market. Unlike in the FOMO-driven 2000s housing market, Zandi doesn’t think speculation is driving our ongoing boom.

That doesn’t mean that interest rate increases are the only problem, or that our market is in the clear. As Dr. Jim Gaines, a research economist at the Texas Real Estate Research Center at Texas A&M, told us earlier this year, employment is the factor to watch:

However, widespread job loss — similar to what we saw at the onset of the pandemic — could create complications for the economy and, in turn, the housing market. Could that cause a bubble? Maybe, Gaines said, especially if marginal borrowers defaulted en masse.