Housing Bubble Ahead? The Dallas Fed Says Maybe, But This Economist Disagrees

Share News:

When I rang up Dr. Jim Gaines, a research economist at the Texas Real Estate Research Center at Texas A&M, it must have been something of a Groundhog Day or déjà vu situation for him. He’d just discussed this same subject with a fellow economist and a room full of Fort Worth real estate professionals.

“The use of the term ‘bubble’ is wrong, in my opinion,” Dr. Gaines said regarding a recent report from the Federal Reserve Bank of Dallas. “Generally, when you have a price bubble, you have price increases that don’t make sense.”

That’s what happened when the bubble burst in 2008, kicking off the Great Recession. In that instance, Gaines reminds us, it was “funny money — where people were able to secure loans they could not afford.”

“The increase in prices was completely artificial,” Gaines pointed out.

Today’s market, on the flip side, is driven by a huge amount of demand outstripping anemic supply and out-of-state and institutional buyers using cash to drive up prices. It was that same housing bubble that put us in our current inventory situation, as builders never fully came back to the market after the housing crash, and when COVID hit, everything was exacerbated.

“That was the last time an oversupply situation existed,” Gaines added.

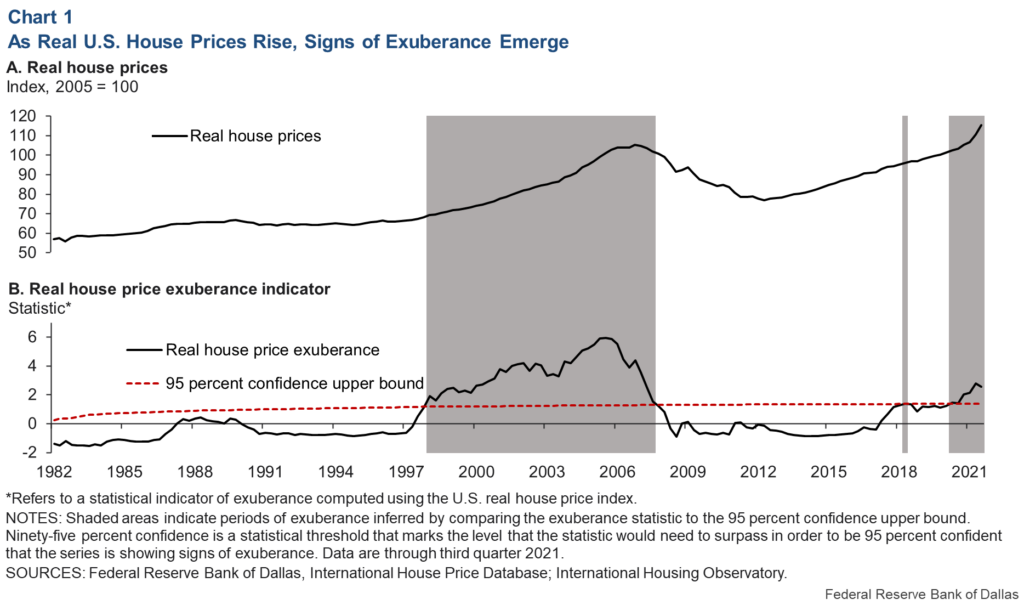

So it was interesting to see a Federal Reserve Bank of Dallas report use the term “bubble” eight times to refer to the market conditions we’re seeing right now.

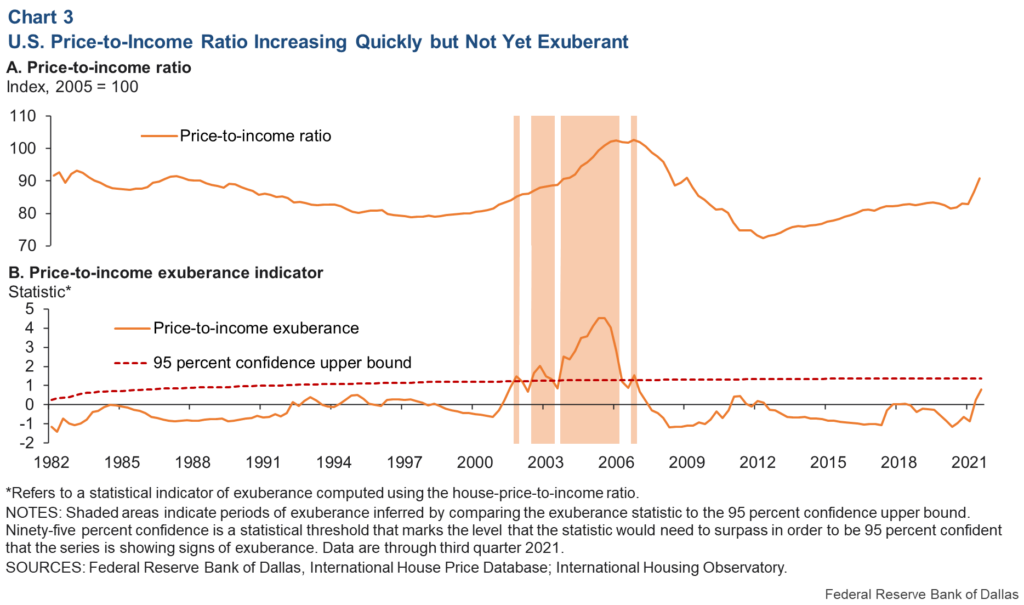

“An asset—in this case, housing—is in the primary expansionary phase of a bubble when price rises are out of step with market fundamentals,” the report laid out. That’s exuberance, according to the Dallas Fed. But are housing prices really that far off?

Considering how loaded the term is, it’s no wonder that the report has gained steam as it traveled through the media mix. However, using “bubble” is rather clickbait-y for shellshocked real estate professionals. It’s certainly going to get you some eyeballs.

That’s not to say there isn’t a significant crisis in our housing market.

“I’ve had people tell me since 2018 that the bubble was going to burst,” said Joanna Gaines Utley (no relation), the team leader of the Land and Luxury Group at Compass Dallas. “Nothing seemed truly unhealthy until January 2022. All of a sudden it was 50-plus offers on a house, houses selling for $100,000-plus over neighborhood comps, and everything under $300k disappeared.”

Her experience isn’t unique, as competition has ramped up over the paltry number of active listings in our region, putting even more strain on an already overheated market thanks to cash-flush out-of-state buyers and investors looking to make a quick buck. But the demand for housing is high and supply is low — basic economics, Dr. Gaines points out — so it would make more sense to track a metric that can show whether the home price increases are all that lofty considering the market conditions.

The Home Price Index from the Texas Real Estate Research Center at Texas A&M University for the Dallas-Fort Worth-Arlington MSA — a true apples-to-apples comparison of the change in the price of a home for sale — increased 23.55 percent year-over-year in the fourth quarter of 2021. It was just a year before that the index sported a relatively modest 7.4 percent increase. For comparison’s sake, the index was -2.02 percent in the fourth quarter of 2008.

More Than One Factor

But the Dallas Fed report did do well to spell out that it’s not just one market factor that can influence the overall economic conditions. In fact, there are several, Dr. Gaines said.

“One of the results of the Great Recession was Dodd-Frank,” he said. “The lending criteria changed — most of the people are borrowing money and have to prove that they will be able to repay it.”

However, widespread job loss — similar to what we saw at the onset of the pandemic — could create complications for the economy and, in turn, the housing market. Could that cause a bubble? Maybe, Gaines said, especially if marginal borrowers defaulted en masse.

Of course, another key factor is interest rates, which are controlled by the Federal Reserve. With inflation on the rise, the Fed just raised interest rates for the first time in more than three years and has signaled that more are coming down the pipe. And as the Fed increases rates, so do lenders. The days of near-rock-bottom interest rates could soon be over.

“Houses under $300,000 — the monthly payments aren’t affordable with the rate hikes,” Utley said. “I really don’t know how single-family income will be able to find affordable housing within a 45-minute drive to Dallas.”

But Dr. Gaines thinks that the rate hikes may be the least of our worries.

“I don’t think that interest rates are going to go up enough to affect demand significantly,” he said, though the Fed is notorious for overreacting.

So is there a bubble? No. But there will be some level of a market correction.

“It’s not a bubble like the one we saw in 2008,” Dr. Gaines said, “but I think that for the rest of this year we will still have a strong market.”