Home Sales Forecast Tempers Amid Mixed Economic Signals

Share News:

Hopes that home sales would really pick up next year alongside a steady decrease in mortgage rates are growing more sober following another revised forecast by Fannie Mae.

For the second month in a row, the government-backed lender’s economic research group toned down its expectations for home sale activity in 2026. In September, a 9.2% increase was apparently in the cards. Then, in October, an 8.9% bump was expected. The latest projection is a 7.3% rise in home sales.

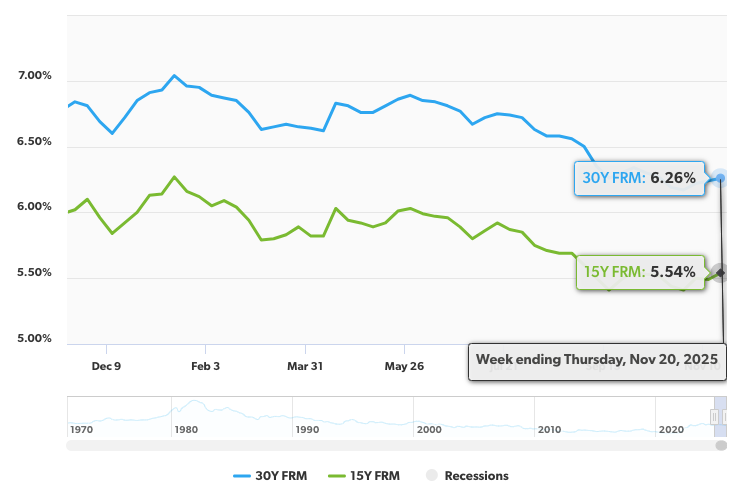

Mortgage rates have been playing ball since the start of the summer, heading downward on the expectation of benchmark interest rate cuts by the Federal Reserve. Two cuts later, though, and it appears they’re stabilizing, with the 30-year pegged at 6.26% as of Nov. 20. And now, it seems a third cut to close out the year is up in the air. Fed officials appear split on the question.

“It’s striking that both sides of the debate have high-conviction compelling arguments — cut based on cooling labor conditions or hold because of lingering inflation risks,” said Ian Lyngen, BMO Capital Markets’ head of U.S. rates strategy, according to Investopedia.

The latest jobs report, which was delayed due to the government shutdown, showed that September beat expectations considerably, adding 114,000 positions. Officials at the central bank had been cutting rates in anticipation of an economic slowdown, but if the economy’s not cooling, there’s less reason to issue another and risk bolstering inflation.

Lawrence Yun, chief economist at the National Association of REALTORS, previously said that several million prospective homebuyers could enter the market if mortgage rates got to 6% or below. While mortgage rates aren’t directly tied to the Fed’s benchmark interest rate, they tend to follow the trajectory.

Earlier this month, before the jobs report was released, Yun predicted that existing-home sales would increase by as much as 14% next year, according to Real Estate News. Fannie Mae’s 2026 projection for existing-home sales is a bump of 7.8%. With inflation hanging around 3%, though, the central bank might be reluctant to put its foot on the gas.

Susan Collins, president of the Federal Reserve Bank of Boston, told NBC News that she saw “reasons to be hesitant.”

“My own view is that policy is currently in the kind of mildly restrictive range after the 50-basis-point easing that we did in September and October, and that’s appropriate,” she said.

Rates aren’t everything though. Home prices are still prohibitively high for many would-be buyers. Things have gotten so bad on that front that the share of homes purchased by first-time buyers has fallen to a historic low of 21% and the median age of first-time buyers rose to 40 years old — an all-time high, per NAR.

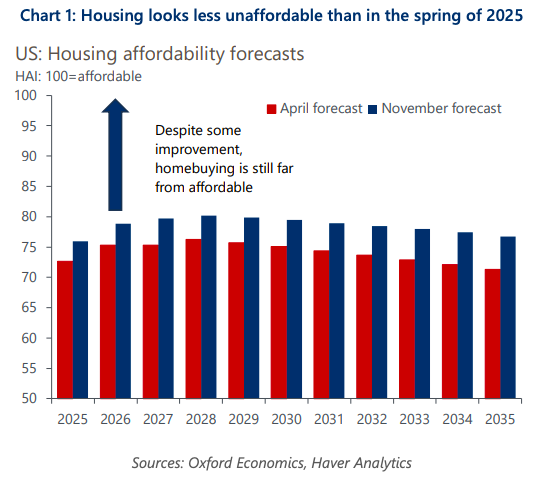

“Our outlook for affordability has improved, largely due to revised assumptions about home price growth. However, barring significant increases in supply, prices would have to decline or mortgage rates would need to fall sharply for homebuying to become widely affordable,” wrote Nancy Vanden Houten, lead economist at Oxford Economics, for a research brief last week.

One has to wonder if the warm bubble bath President Trump took with New York City Mayor Elect Mamdani is going to have an effect on relocations from the more social destinations of the nation towards a more conservative Texas and South in general. Will desperate people start holding off voting with their feet. One can see a conflict in Trump as he seems torn between making America great again and always keeping New York City great no matter the cost. As one can take the boy out from New York City, can one take the New York City out from the boy?

Stay tuned . . ..