Private Flood Insurance Providers Keep Closings Afloat During Government Shutdown

Share News:

The longest government shutdown in U.S. history might soon be winding down, and while a lot of attention has rightfully been focused on lapses in SNAP benefits and air traffic control staffing, a real estate dimension has been quietly flying under the radar: flood insurance.

Several decades ago, the private market wasn’t offering much in the way of flood insurance. Even today, most standard homeowners’ insurance policies don’t cover flood damage. In 1968, the National Flood Insurance Program (NFIP) was created to fill the need, offering federally backed policies to homeowners, renters, and businesses in exchange for jurisdictional adoption of certain flood plain management rules.

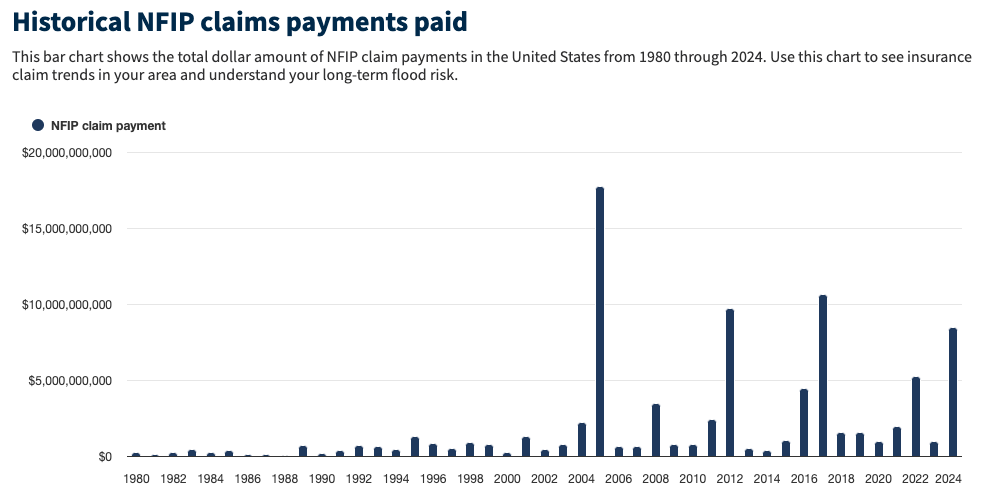

As of December 2024, NFIP had over 4.7 million policies in place valued at more than $1.3 trillion in coverage — with $3.4 billion in authorized funds to pay claims. It’s the biggest provider of flood insurance in the country.

Obviously, not everyone really needs flood insurance. However, it is required whenever a federally backed lender makes a loan for a property located in a special flood hazard area. This applies to mortgages issued by or through Fannie Mae, Freddie Mac, the Federal Housing Administration, the Department of Veteran Affairs, and the Department of Agriculture.

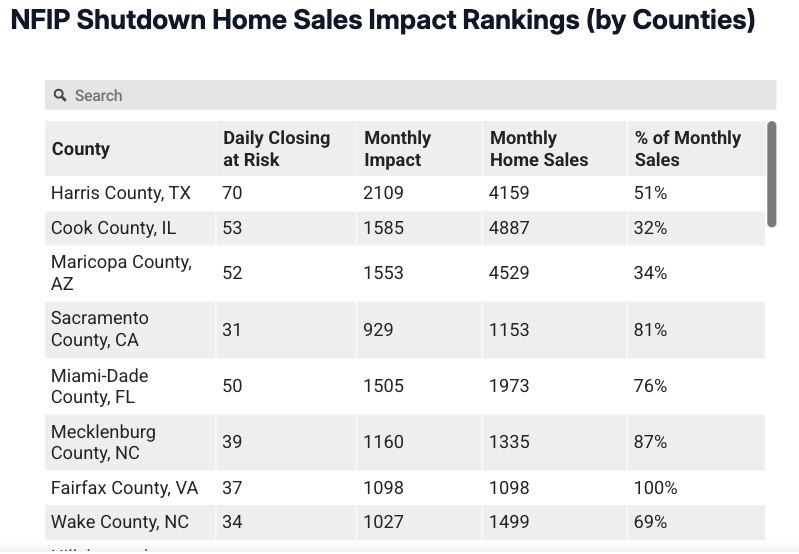

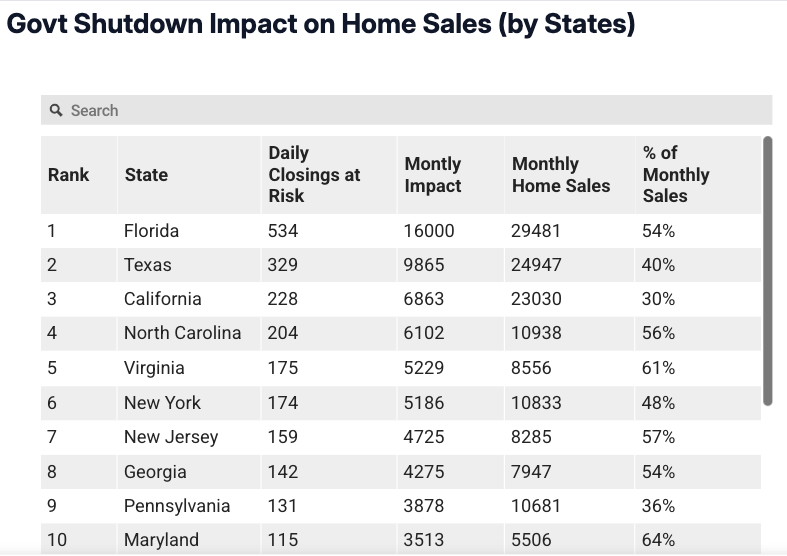

Now, around the time the government shutdown began in October, property technology company HomeAbroad dropped a study ranking counties and states by how many home purchases were at risk due to the suspension of the NFIP. Among counties, Harris County ranked first, and Texas ranked second among states behind only Florida. The numbers were startlingly high, but that might be because the methodology didn’t appear to control for cash deals. Regardless, it gives you a pretty good idea of where you’d expect issues to arise during a government shutdown based on flood-prone areas and home sale activity.

“It’s absolutely causing an impact more from an approval perspective, being able to get federal flood insurance policies not just underwritten and bound but updated as well, so even refinance customers are being impacted,” HomeAbroad director of mortgage sales Steven Glick told CandysDirt.com. “I just had a client close this week where they had an [NFIP] policy bound, and they needed updates. They had to go and find an alternative private policy in order to be able to close on the purchase of their loan.”

Federal guidance was issued to lenders at the start of the shutdown, though, allowing them to issue mortgages without requiring flood insurance. It’s unclear how many have taken that risk. Otherwise, it’s been the private market for those making deals.

“The shutdown has effectively served as a live test for the market, demonstrating that even without the NFIP, the housing market continues to function and that flood insurance remains readily available through private carriers,” said Matt Duffy, president and chief risk officer at Neptune Flood.

Duffy’s company is the largest private flood insurance provider in the United States. He told CandysDirt.com that the federal guidance dampened increased activity in the private sector but risked expanding the existing flood insurance gap.

“Only about 2% of properties nationwide carry flood insurance, and even in high-risk states like Florida, that figure is just 13%. The same dynamics have been seen in Texas and Louisiana, where interest in private flood coverage remains strong but the federal guidance has similarly limited potential growth,” Duffy said.

True enough, fear of deals falling through may have been unwarranted. CandysDirt.com spoke with Houston Association of REALTORS board member Bill Baldwin, owner of Boulevard Realty. He said this go-around has been nothing like the last shutdown in 2018-2019, at least not in the Houston area.

“We really haven’t seen the disruption we anticipated,” he said, noting that a lot of professionals in the industry saw the writing on the wall politically and planned ahead, essentially expecting a shutdown of some duration. But more importantly, private flood insurance has grown its footprint.

“I’ve been in real estate 28 years. Private insurance is much, much, much easier to get today, much more affordable today, and much more available,” he said.

Baldwin explained how private flood insurance used to be limited to high-end properties (NFIP policies max out at $250,000 for a residence and $100,000 for its contents). Now, homes are generally more expensive, and private insurance is more accessible, even as the cost of insurance has risen overall. And, of course, lots of potential policyholders can’t break into the housing market because of where home values are at. For those who can, though, there are now plenty of options.