DFW CRE Flexes in Industrial and Retail While Office Buckles

Share News:

With 2025 behind us, we’re getting an idea of how Q4 panned out on the commercial real estate front in D-FW. To nobody’s surprise, the office sector lagged behind retail and industrial once again, but tenants are still paying up for high-quality Class A space as rents keep rising, according to Partners Real Estate, which recently dropped its CRE market reports for the quarter.

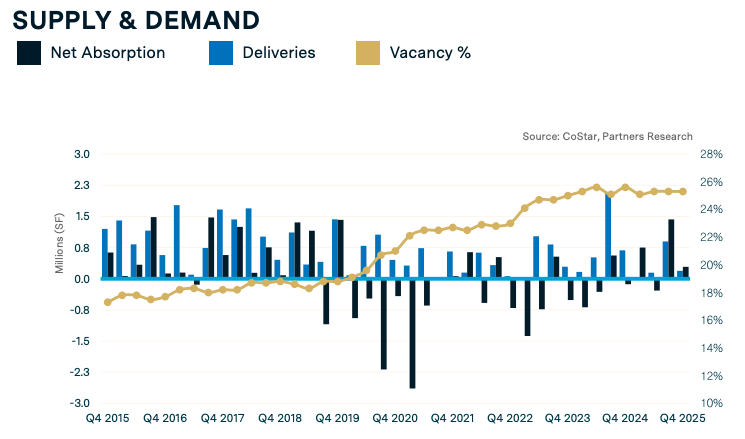

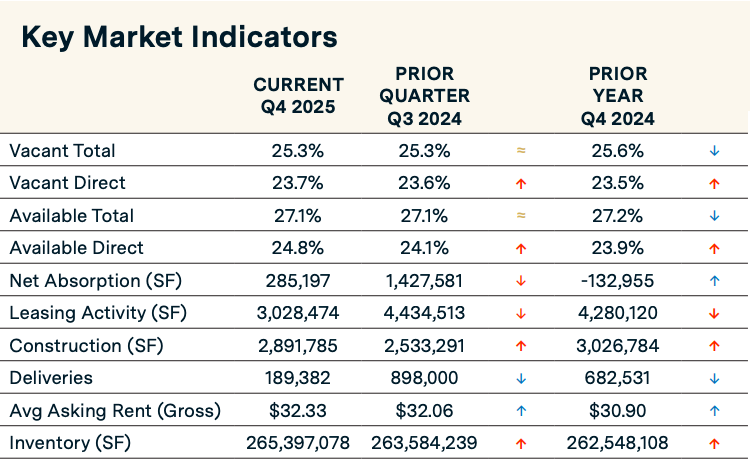

Leasing activity saw a steep 31.7% drop from the third quarter, and net absorption fell by roughly 80% over the same period, decreasing from about 1.4 million square feet to a little over 285,000 square feet. Total vacancy stood flat at 25.3%.

It is what it is when it comes to office space these days. Hybrid and remote work arrangements seem to have dealt the sector a sustained blow following the COVID-19 pandemic, reducing the amount of square footage employers need. Companies are also prioritizing flexibility and higher-quality environments, reshaping demand and leaving traditional office layouts increasingly out of step with modern work.

New suburban campuses and mixed-use buildings in popular neighborhoods appear to be the way of the future. To add a finer point to it, a half-empty, 36-story downtown Dallas office tower built in the early 1980s that was put on the auction block last year has seemingly failed to receive an acceptable bid, despite its conversion potential, per The Dallas Morning News.

Flight-to-quality isn’t letting up, though. Class A office space logged positive absorption, unlike Class B properties, which went negative last quarter. Class A also logged record-high rents, coming at $36.20 per square foot on average. Across the whole Metroplex, the average gross rental rate was $32.33 per square foot, up 0.8% from the previous quarter and up 4.6% from Q4 of 2024.

“The Uptown/Turtle Creek submarket boasts the highest rental rates, with the overall average gross rent currently sitting at $62.10 per sq. ft. The lowest rental rate in the Stemmons Freeway submarket is $21.46 per sq. ft.,” the Partners office report reads.

No surprise coming out of Uptown, which has become Dallas’ premier work, play, live neighborhood.

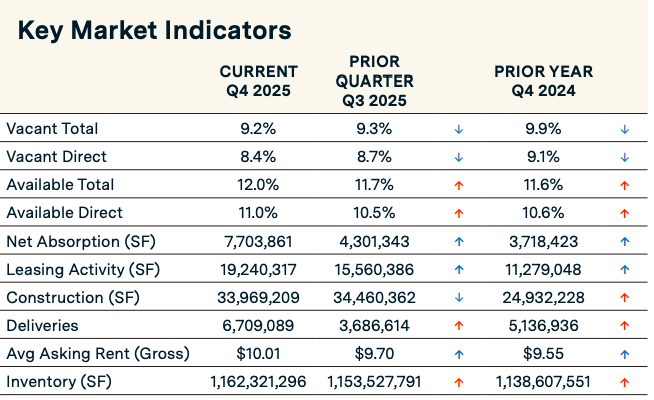

Landlords hawking office space might be crying the blues, but not so much in the world of industrial. The industrial sector remained one of the region’s strongest performers, buoyed last quarter by robust leasing and absorption despite all the new supply.

Developers delivered 6.7 million square feet in Q4, clocking an 82% increase from Q3 and 30.6% from Q4 of 2024. This had the effect of keeping vacancy elevated at over 9%, even though leasing activity came in with a 23.6% quarter-to-quarter increase and a steep 70.6% year-over-year spike. Warehouse and distribution facilities drove much of the activity, and asking rents continued to climb, reflecting long-term confidence in North Texas’ logistics advantages.

“The Northwest Dallas Outlying and DFW Airport submarkets currently have the highest overall average rates at $19.13 and $12.87 per sq. ft., respectively,” the industrial report reads.

As previously reported by CandysDirt.com, industrial properties have been a driver of Dallas’ CRE tax base, with the northwestern part of the city attracting significant attention from developers.

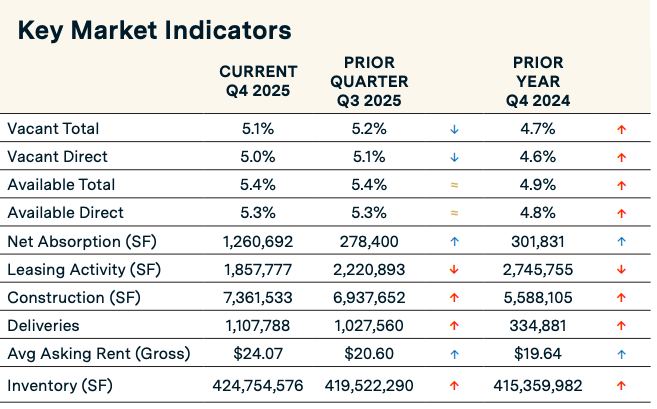

Retail showed similarly solid fundamentals across the Metroplex. Vacancy stayed low at 5.1%, and net absorption rose sharply, jumping from around 278,000 square feet in Q3 to 1.26 million square feet in Q4. Rent growth also accelerated, with asking rents posting significant year-over-year gains of roughly 22.6%.

“The submarkets with the highest rental rates include North Central Dallas ($29.31 per sq. ft.), East Dallas Outlying ($28.89 per sq. ft.), and Central Dallas ($27.59 per sq. ft.), which are well above the metro average. In contrast, the lowest-asking-rent submarkets include Southwest Dallas ($16.18 per sq. ft.), Central Fort Worth ($17.28 per sq. ft.), and Southeast Dallas ($17.40 per sq. ft.),” the retail report reads.

All this growth is going on and the office sector just can’t catch a break. Maybe 2026 will see some sort of radical change that puts people back in cubicles. But maybe more likely, the increased deployment of artificial intelligence will make things even harder as businesses shed staff. Yikes.