Both Sides of the Aisle Don’t Understand Housing Affordability

Share News:

By Jonathan Miller

Special Contributor

Takeways

- The proposed federal ban on large institutional investors buying single‑family homes targets big funds and REITs, not small landlords, but would likely have little real impact on affordability or inventory.

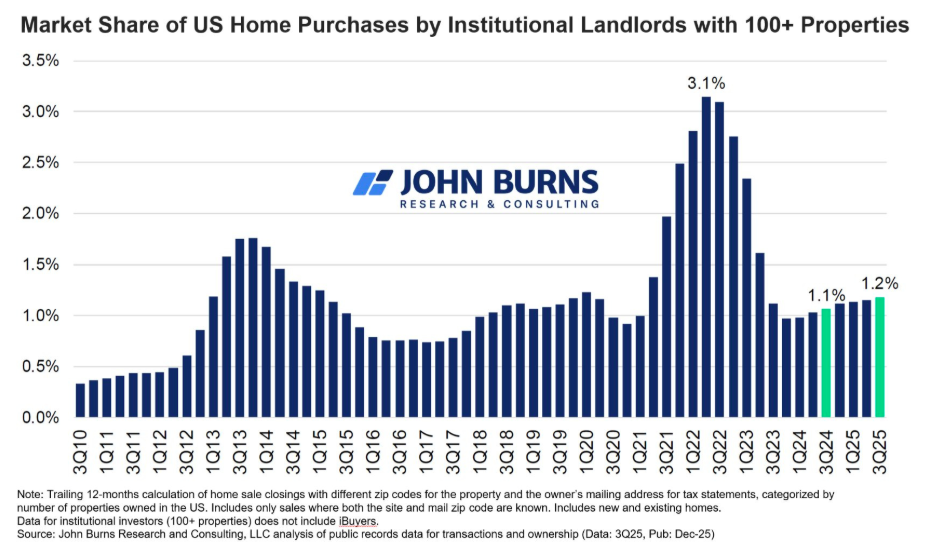

- Institutional owners represent only about 1% of U.S. homeowners — with Blackstone holding just 0.06% — and are most concentrated in Southern and Sunbelt markets where supply is already higher.

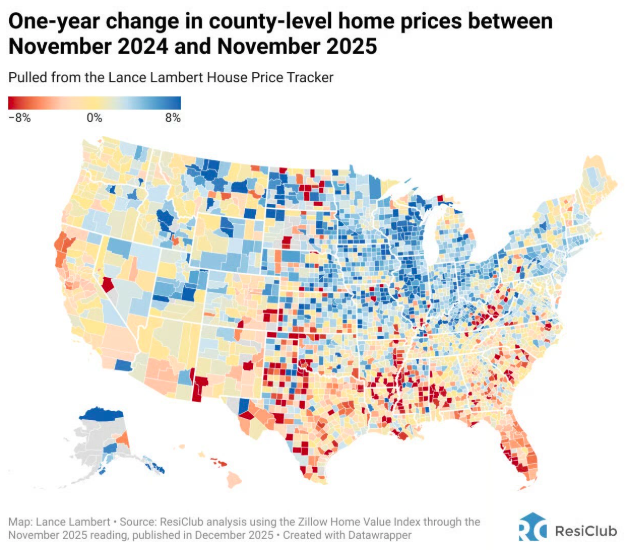

- Price trends show no clear link between institutional ownership and housing cost increases; in fact, prices are falling in regions with the highest levels of such ownership.

No Apparent Connection Between Affordability and Institutional Ownership

The administration has said it is “immediately taking steps to ban large institutional investors from buying more single‑family homes” and will ask Congress to codify the policy, emphasizing that “people live in homes, not corporations.” Conceptually, the ban targets private‑equity funds and REITs above certain size thresholds, not small landlords or typical local investors, who account for more than 90% of investor properties. The only benefit to Main Street seems to be a possible nominal removal of cash buyer competition in some specific small markets. One question that has come up about the president’s potential ban is whether it will apply only moving forward or require a sell-off of their existing housing stock. No details are available yet.

I was invited to join Scarlet Fu on Bloomberg Television’s Markets program [the other day] to weigh in on the president’s recent comments about taking steps to ban institutional investors from purchasing single-family homes. This seemingly random pronouncement was tied to his comments [in December] calling for bold reform of the housing market. This particular announcement was decidedly anti-Wall Street, as captured in the terrific Bloomberg piece Trump Bid to Ban Corporate Homebuying Blindsides Wall Street (gift link).

And we’ve seen this type of anti-Wall Street pronouncement before on the other side of the aisle by U.S. Senator Elizabeth Warren back in 2019. If you recall, Wall Street swooped in during the U.S. foreclosure crisis (2009-2013) to buy foreclosed houses. In response to Warren’s claims that they made shameless profits back then, Wall Street contended that it helped stabilize neighborhoods after the foreclosure crisis by buying distressed properties when few other buyers were available.

The 1% Gets Outsized Attention

As I mentioned in the Bloomberg interview, large landlords have long been a small share of U.S. homeowners. While I certainly get the Main Street versus Wall Street sentiment, the basic fact is that institutional homeowners account for about 1% of U.S. homeowners. Blackstone points out that it currently owns only 0.06% and has cut its position by 20%. But the frustration with consumers and politicians is that financial markets are forward‑looking and price in expected conditions 6–18 months ahead, while Main Street sentiment largely reflects how conditions feel today or over the next few months. In other words, it looks like Wall Street may be moving on.

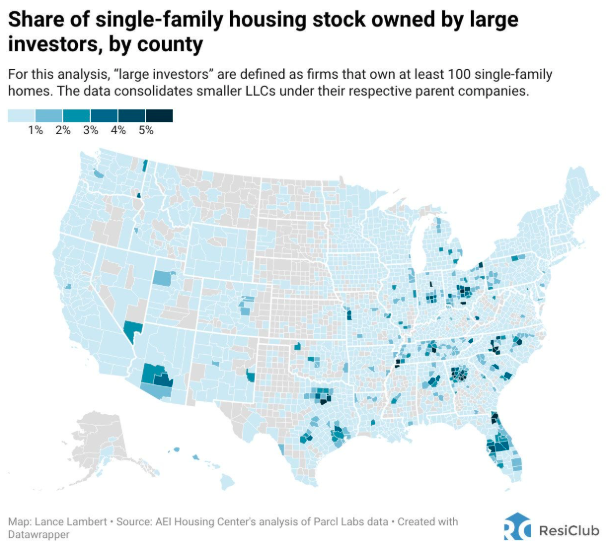

The irony of the attacks on institutional investors is that, according to ResiClub (a terrific publication I subscribe to), their largest concentration seems to be in the South and Sunbelt, where listing inventory is now the highest. Of course, that wasn’t the case 15+ years ago when this whole thing started. The irony here is that the long, inaccurate narrative has been that institutional investors gobble up most of the inventory, which is a key reason prices have risen so sharply coming out of the pandemic. In the past few years, supply in the region has surged, and removing these investors is not expected to have any beneficial impact to most local housing markets in the context of enhancing affordability.

Of course, institutional investors (Wall Street) are equal opportunity offenders by all accounts when it comes to Main Street storylines. The Midwest has very limited inventory, but institutional investors also have a concentration of houses there, and prices are rising.

Prices are up in the Northeast and Midwest but down in the South, where institutional single-family ownership is at its highest.

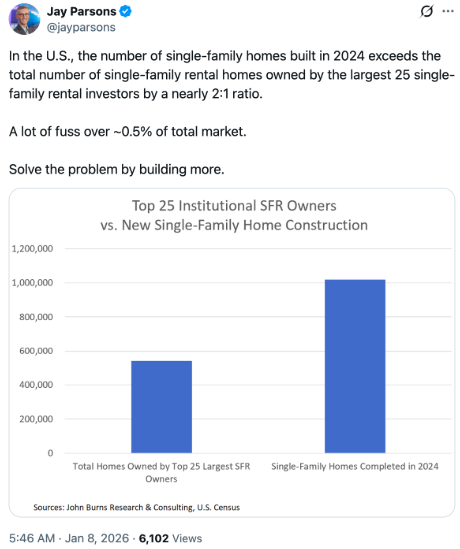

New Homes Account for Tiny Slice of Institutional

Even in the new homes sector, the market share is even smaller, making this ban disconnected from the affordability problem.

Final Thoughts

The administration’s proposed ban on large institutional investors buying single-family homes aims to curb Wall Street’s role in housing, but evidence shows little connection between institutional ownership and affordability. Big investors, such as private equity firms and REITs, represent only about 1% of U.S. homeowners — Blackstone’s share alone is just 0.06%. Their holdings are concentrated mostly in the South and Sunbelt, where inventory is relatively high and home prices have actually fallen, undermining claims that these investors drive housing costs higher. With most investor-owned homes held by small, local landlords, the proposed restriction is unlikely to meaningfully improve affordability or housing supply.

Neither side of the political aisle seems to know what to do about affordability other than calling out the boogie man. Well, the first thing to do is build more housing starting now.

The Actual Final Thought – Back in 1995, I bought this at a long-ago store next to my old office on West 38th Street in Midtown, Manhattan (I think it’s now a Chipotle, and my office building has been torn down), only because I liked the cover of the cassette box (remember those days?) I then proceeded to wear it out. The band’s name seems appropriate today, and, given the song’s title and lyrics, suggests a simplistic narrative that doesn’t align with reality.

Jonathan Miller is a housing analyst and professor at Columbia University. He is a syndicated columnist of “Housing Notes.”