Final Thoughts on 2025: Sure Glad It’s Over

Share News:

By Jonathan Miller

Special Contributor

- Inflation and mortgage rates remain as risks, with modest rate relief expected next year and potential tariff-related court rulings adding upside and downside volatility to borrowing costs.

- Manhattan’s luxury sales prices have structurally detached from the broader market over the past two decades, while luxury rentals have not.

- Building more high-end apartments is helping push down rents for older units, and wage growth is still slightly outpacing inflation reducing financial stress on households.

2026 Looks To Be A More Active Year For The Housing Market

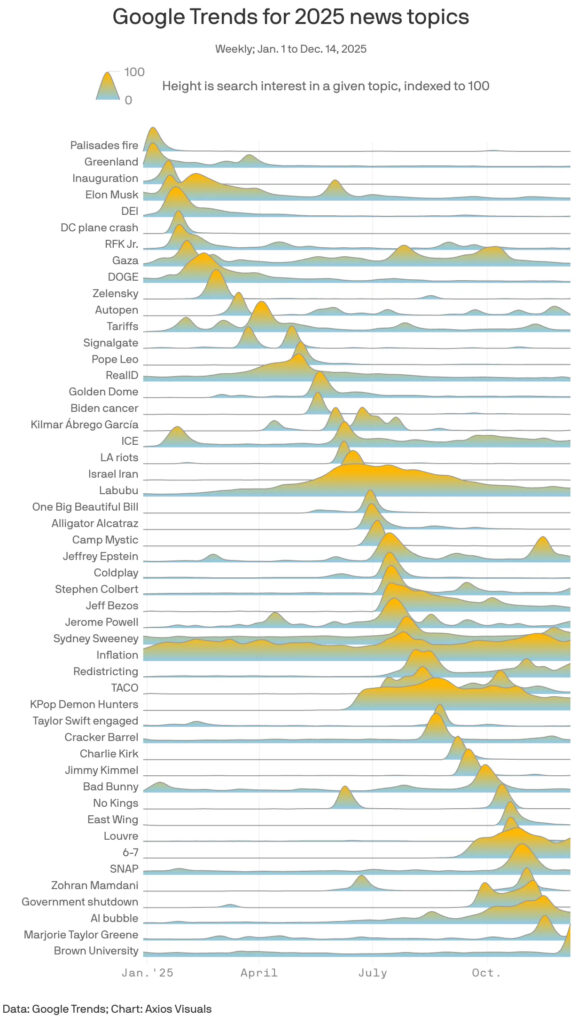

Inflation, which housing accounts for a third of its calculation, has been a consistent topic throughout the year, as shown in this incredible AXIOS visualization.

Mortgage rates are expected to fall a little next year, while markets are betting the Fed will cut rates only once or twice. The inflation threat remains a concern, but if the Supreme Court finds that the president, rather than Congress, applied tariffs unconstitutionally, that could mean even deeper cuts and potentially lower mortgage rates. Ha. In a world at peak cynicism right now, don’t hold your breath. In fact, we could see mortgage rates tick up initially if the Supreme Court renders such a decision.

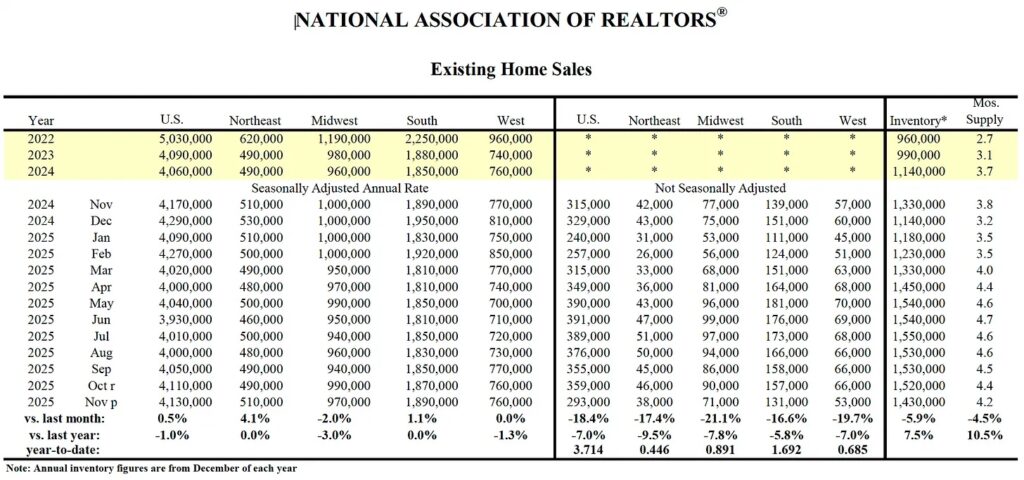

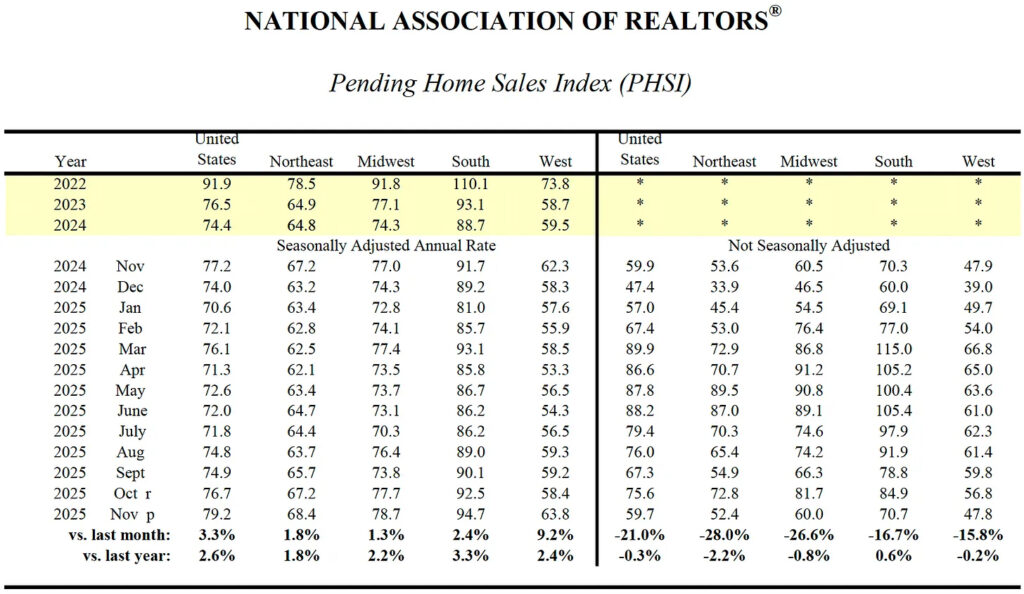

In reference to NAR’s data releases, I think it’s more realistic to look at non-seasonally adjusted year-over-year sales levels (the right side of the following tables). I’m not sure why there needs to be a seasonal adjustment for year-over-year comparisons, since such an adjustment already controls for seasonal patterns, but hey, I’m not a trained economist, just a battle-tested market analyst.

Existing Home Sales For November 2025 YOY -7% (not seasonally-adjusted)

Pending Home Sales For November 2025 YOY -0.3% (not seasonally-adjusted)

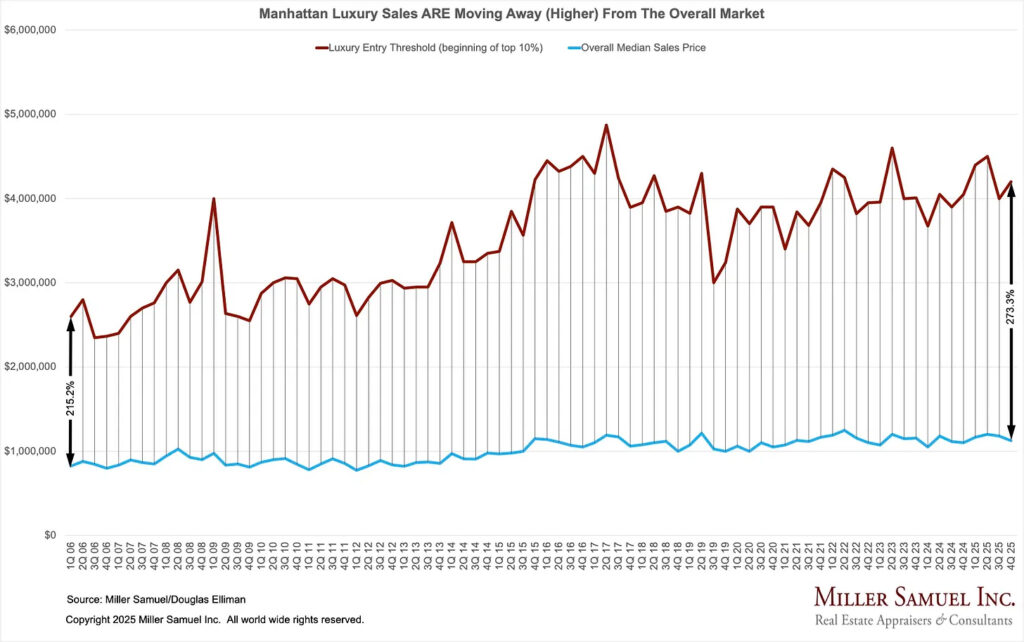

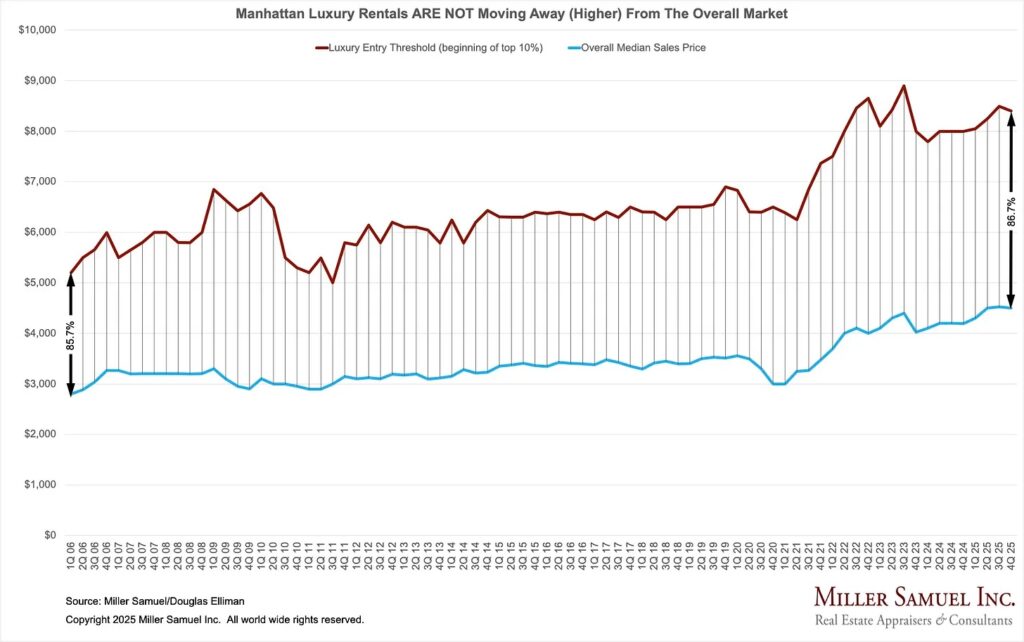

High-End Sales Prices ARE Detaching From Overall Market (In Manhattan)

I took a look at Manhattan housing prices over the past two decades to help visualize the relationship between the high-end housing market (top 10% aka “Luxury”). To illustrate, I looked at the median sales price of co-ops and condos (which account for about 98% of residential sales each year). To measure the disconnect, I also trended the entry price threshold for the top 10% of the market (essentially the bottom of the top 10%). Over the past decade, the high-end market has been moving further from the remainder. As a percentage, the luxury market’s distance from the overall market’s median has widened by 58.2%.

This is consistent with why we see a lot of super luxury sales (≥ $50 Million) across the US, as they are essentially fully detached from their respective local housing markets. I worked with a large media outlet on the super-luxury market for a story coming out on January 1, and I will be writing about it with lots of charts to recap the year. Since this is a small submarket that tends to see a burst of closings at the end of the year, the analysis won’t be available until the first.

In contrast, the rental market is NOT seeing the same pattern in the chart below. In fact, there is barely a difference in the spread between the bottom of the luxury rental market and the overall median rent over the past two decades. Crazy, right?

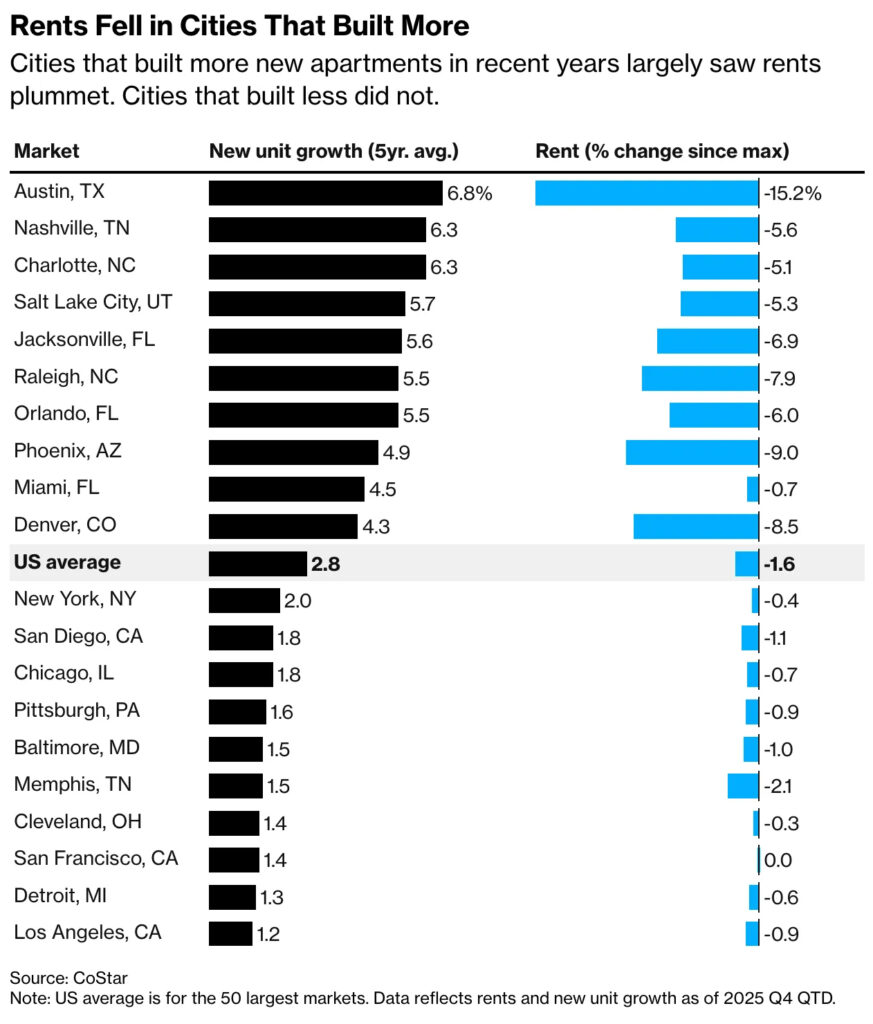

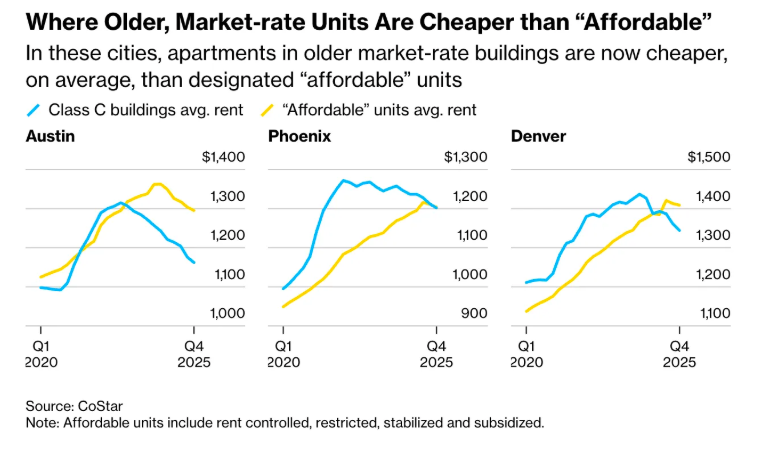

Build More Luxury Apartments To Lower Rent

While US construction in the apartment market is biased towards the higher end due to the still-high cost of land, labor, and materials, it is not correct to say (as I have sometimes said) that we are building the wrong type of housing. This excellent Bloomberg piece tells us why: Luxury Apartments Are Bringing Rent Down in Some Big Cities (gift link). When overbuilding higher-priced rentals, think of a layer cake (when I’m not telling you to think about why pie>cake). The top layer melts into the next layer below it, competing with the existing product. That product melts down to the next layer and competes with the existing product there, and so on. In other words, while not a perfect, fool-proof solution, “build more housing” still makes sense.

The craziest part of the Bloomberg piece was the idea that older market-rate apartments have become cheaper than “affordable” apartments. In other words, build more apartments, even if they are “luxury apartments.” Why? Because many of the existing tenants move into the new product, freeing up the lower-priced product.

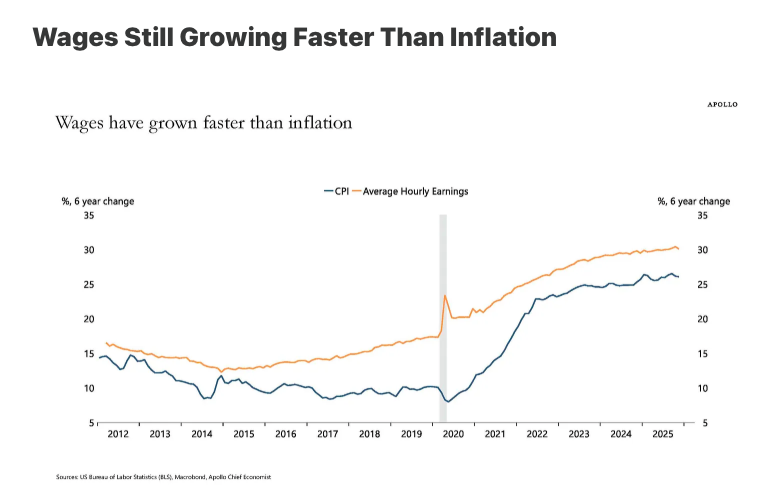

As many of us continue to scratch our heads on how consumers can afford higher inflation, rents, healthcare, etc., the simple answer is that they really can’t in the long run. However, the fact that wages are still outpacing inflation helps reduce the pain a bit.

Final Thoughts

Apologies for the monster read! Inflation and mortgage rates remain key risks, with only modest rate relief expected next year and tariff-related legal uncertainty potentially adding volatility. Existing and pending home sales are still lower year over year, while Manhattan’s luxury sales prices have sharply detached from the broader market even as luxury rentals have not.

What have we learned here about improving affordability of housing? Build more of it.

See you in 2026!