Hawks and Doves: A Lot More Rate Cuts Will Probably Hurt Housing

Share News:

By Jonathan Miller

Special Contributor

- Neil Young’s Hawks & Doves serves as a metaphor for a divided, less inspired era, paralleling today’s economic volatility and the expectation of only modest mortgage rate cuts next year.

- The Federal Reserve’s internal split — hawks resisting further rate cuts and doves urging more easing — reflects rising political pressure, tariff-driven inflation, and fading public confidence in the Fed’s independence.

- Tariffs and inflation continue to erode affordability, hitting lower- and middle-income households hardest, while luxury housing shows relative resilience as policymakers struggle to balance growth and inflation control.

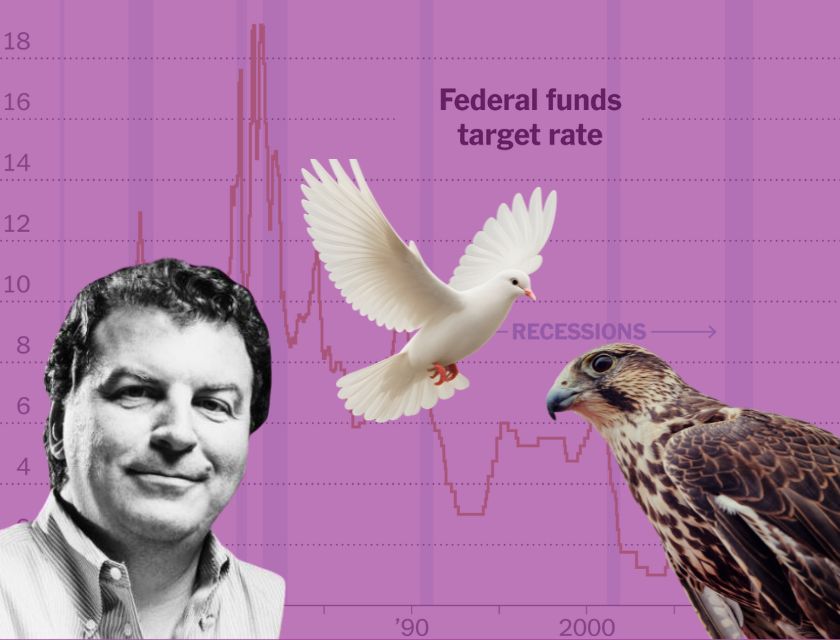

The Fed Cuts And The Search For A Heart Of Gold

Neil Young’s 1980 political album Hawks & Doves was disappointing to his fans after the barn-burner Rust Never Sleeps and the classics After the Gold Rush and Harvest set the standard. For me, the Hawks & Doves album symbolized the beginning of a weaker era of his albums and perhaps, by extension, today’s housing market. As I’ve long said here in these Housing Notes, I yearn to bring back boring economic policy. The rapid economic ebbs and flows of the past couple of decades may further deter first-time buyers from entering the market and erode their confidence in housing as an asset class.

Admittedly, my personal favorite Neil Young song is the storytelling on his 2003 Greendale album, described in Wikipedia as “Greendale combines numerous themes on corruption, observation of the passing of time, environmentalism, and mass media consolidation.” The storytelling really works if you live in it for the entire album — it’s just brilliant — and doesn’t get enough appreciation even though he wrote a follow-up to it, Return to Greendale.

But I digress…

Young’s Hawks & Doves album popped into my head as I was thinking about the expected uptick in Federal Reserve policy infighting over the next few years. The idea of a divided Fed likely means lower market confidence in the institution, depending on how the infighting plays out. The very title “Hawks & Doves” illustrates that Fed policy is rarely one‑sided; even in easing cycles, there is a tug‑of‑war between doves who want to move faster and hawks who fear losing inflation control.

I don’t envy the Federal Reserve Chair right now. Powell is a lame duck because the president, also a lame duck, wants to replace him at the end of his term in May to push interest rates lower. Portions of the economy are faltering now, and tariffs are the key reason, so he needs to address the falling affordability. A newly appointed Fed chair doesn’t have the power to immediately pivot the Fed to a more dovish stance, but he does have influence to build consensus over time. The existing Fed is quite mixed in its policy stance, but the administration will work hard to tilt it toward greater dovishness.

A Tariff Refresher

Tariffs are the cornerstone of the new administration’s economic policy, but they are inflationary, and without them, I suspect interest rates would already be lower. The Supreme Court is debating the constitutionality of the president’s current tariff implementation rather than Congress’s. But based on their susceptibility to political pressure, don’t hold your breath. The recent bailout proposed to US Farmers illustrates how fundamentally damaging tariffs are in the short term, but especially over the long term, as international buyers of US crops switch to other source countries for greater reliability. Also, please note that Commerce Secretary Lutnick has virtually disappeared from his role as tariff cheerleader in recent months, reappearing only for damage control.

What The Hawks Want

Hawkish officials argue that most of the heavy lifting on cuts is done and want to slow or stop easing to avoid re‑igniting inflation. They point to still‑elevated inflation versus the 2 percent target and worry that easier policy, on top of previous cuts, would overstimulate already resilient demand. Several regional Fed presidents have either dissented or signaled they could oppose further cuts.

What The Doves Want

Dovish officials are more focused on labor‑market softening and downside growth risks, arguing for additional cuts to cushion a weakening jobs backdrop. They see the recent reductions as necessary to prevent an unnecessarily sharp slowdown and emphasize that policy remains restrictive even after a series of 25‑basis‑point moves. Doves are also more willing to tolerate modestly above-target inflation if it helps stabilize employment.

Cost Inflation Versus Income Inflation

Cost inflation (what is happening now) refers to how fast the prices of what you buy are rising, while income inflation (what happened during the pandemic) refers to how fast your pay or other income is rising. The gap between the two determines whether your real standard of living is rising or falling.

Cost inflation is usually measured by price indexes such as the Consumer Price Index (CPI), the Personal Consumption Expenditures (PCE) index. This is what most consumers are focused on now. Grocery bills and daily expenses are much higher this year because of tariffs.

Income inflation is the rate of change in your nominal income (wages, salaries, etc.), before adjusting for inflation. Wages seem to be rising faster than inflation.

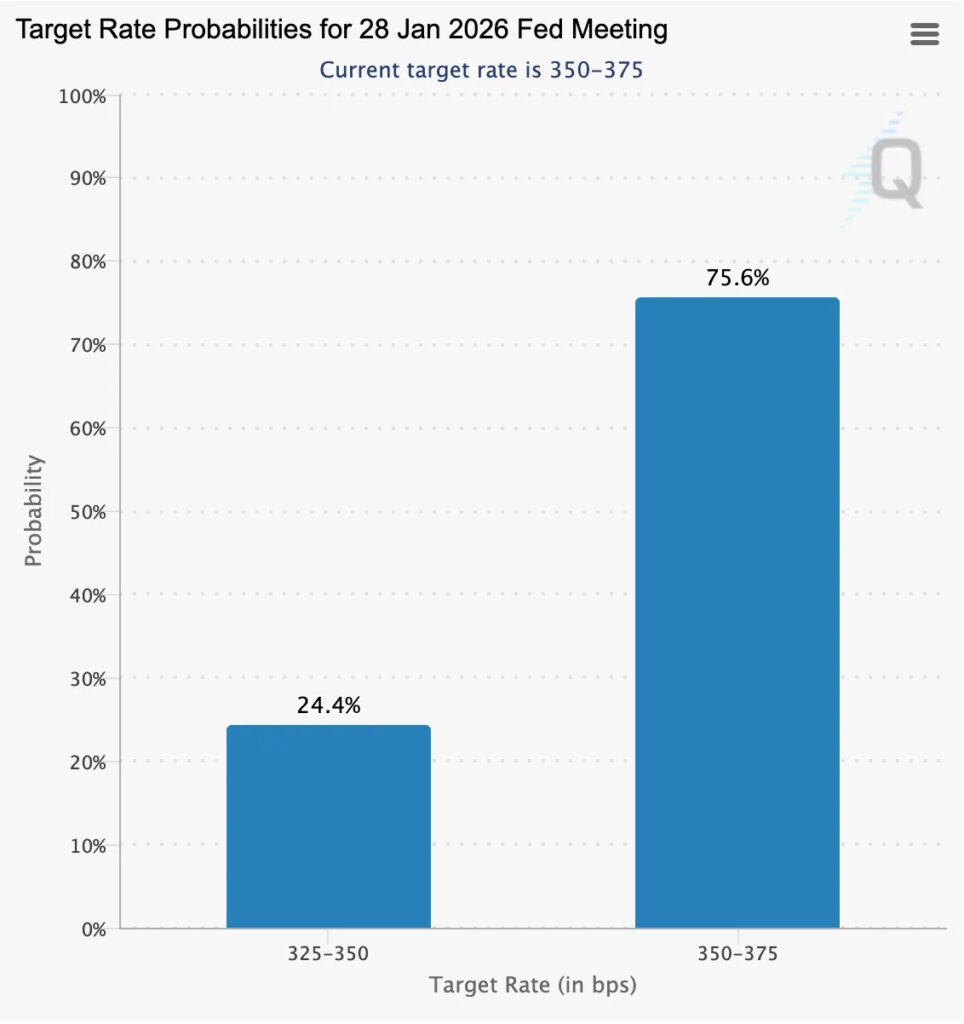

CME Futures

The CME is a great place to understand how financial markets view future Fed rate changes. This is done through the futures market — what investors are thinking. The current odds are 3-to-1 against a rate cut in January, and Powell suggested only one rate cut in 2026.

With Chairman Powell’s term ending on May 15, 2026, the financial markets will probably expect an eventually more politically-influenced dovish policy stance. The part missing from the political meddling with the Fed is that it will probably work against consumers. The tariffs and more significant rate cuts pushed by the administration probably likely won’t translate into significantly lower mortgage rates for housing. Higher inflation will sap consumers’ buying power, something already being felt across the economy.

The hawk/dove split and the administration’s pressure together will increase the odds of more dissent within the Fed and more volatile forward guidance. In the real economy, borrowers may get a little relief, but the Fed’s desire to retain inflation‑fighting credibility limits how far it is likely to go amid further deterioration in jobs or growth data.

If the administration’s goal is to lower interest rates, which could eventually lower mortgage rates, then using a political show of force by attacking the Fed probably won’t yield the results they want.

Luxury Housing Is Showing More Relative Strength

Lower‑ and middle‑income households often face more impact from higher cost inflation because a larger share of their budgets goes to necessities like rent, food, and energy, which have seen outsized price increases. Tariffs are and will continue to have a greater impact on these consumers. This is a key reason why higher-end housing markets and home builders like Toll Brothers, which focus on luxury, are faring better than the rest.

Final Thoughts

I see Neil Young’s Hawks & Doves as a metaphor for the current economic landscape, a symbol of decline following a period of clarity, much like today’s volatile, politically influenced economic policy. The Federal Reserve faces internal conflict between hawks focused on restraining inflation and doves advocating more aggressive rate cuts to support weakening growth, all while tariffs keep prices elevated. Political interference and inflationary pressures threaten to erode public trust in the Fed and limit the benefits of easier policy for consumers. As a result, affordability continues to deteriorate for lower- and middle-income households, while luxury housing markets remain relatively resilient amid the turmoil.

For my Housing Notes readers, this note comes across as super wonky, but the goal was to talk about how the over-eagerness to cut rates too quickly actually works against the best interest of buyers in the housing market. A big takeaway from the Fed keeping interest rates too low for too long during the pandemic is that it led to rapid housing price increases. If rates fall quickly, housing prices will surge again. That’s not an optimal outcome. Selling off listing inventory faster than it could be returned caused a price run-up.

The Actual Final Thought – This is the best way to think about the topic of tariffs (NSFW).

Jonathan Miller is a housing analyst and professor at Columbia University. He is a syndicated columnist of “Housing Notes.”