The Fed’s Rate Cut Is Welcome, But Is It Enough To Reinvigorate the Housing Market?

Share News:

The Federal Reserve lowered the benchmark interest rate for the first time in nine months on Wednesday, offering a glimmer of hope to homebuyers and industry professionals who have been waiting on the central bank to make things easier on borrowers.

Federal Open Market Committee (FOMC) members voted 11-1 to implement a quarter basis point cut, which Chair Jerome Powell characterized as a “risk management cut” following disappointing labor market reports this summer.

As previously reported by CandysDirt.com, Powell and the committee’s majority have refrained from reducing rates the last several FOMC meetings over fears of tariff-driven inflation. Now, committee members are having to balance that still very real threat against a significant slowdown in hiring.

“The labor market is softening, and we don’t need it to soften anymore [and] don’t want it to,” Powell said, according to CNBC.

Lowering the benchmark interest rate is one of the Fed’s main tools for countering a sluggish labor market. By making money cheaper to borrow, the central bank enables businesses to boost spending and investment, facilitating more hiring and economic activity.

The Fed also signaled that there could be as many as two more cuts later this year and another one in 2026. The benchmark now sits at 4.0-4.25%.

How the Fed’s Rate Cut Will Likely Impact Mortgages

The benchmark interest rate directly impacts short-term borrowing costs, while mortgage rates are more closely tied to 10-year U.S. Treasury yields. Because investors see Treasuries and mortgage-backed securities as similar long-term investments, mortgage rates tend to move in step with Treasury yields.

That being said, the Fed influences mortgage rates by shaping economic expectations. When the central bank raises or lowers its benchmark rate, it signals how it views inflation and the broader economy. Higher rates often push Treasury yields up as investors anticipate tighter monetary policy, which in turn leads to higher mortgage rates. On the flip side, when the Fed cuts rates to stimulate growth, yields often fall and mortgages go down with them.

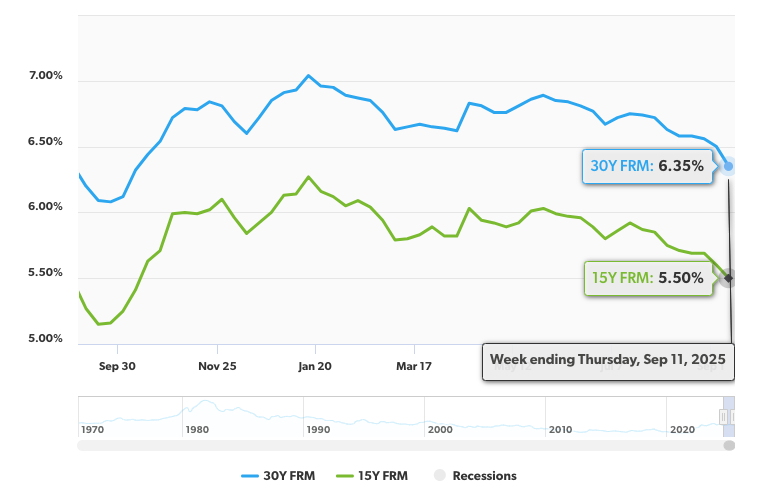

The 30-year was sitting at 6.35% as of September 11, 2025, coming down about half a percentage point as anticipation of renewed rate cuts grew over the summer.

“It seems the anticipated drop has already been helping the residential market over the last few weeks,” Christie’s International Real Estate | @Properties Lone Star CEO Jerry Mooty Jr. told CandysDirt.com. “The hope is this will continue to allow the mortgage companies, and lenders in general, some relief that can be passed on to the buyers.”

Mortgage rates haven’t been all that friendly the last three years, with the 30-year hovering between 6% and 7% since September 2022. The cost of borrowing has kept a lot of would-be homebuyers out of the market, though limited housing stock and swelling home valuations may be the real culprit on the affordability front.

“We are reading that mortgage applications are spiking, so that indicates buyers are getting ready, which is great news for our agents,” Mooty said.

Don’t Uncork the Champagne Just Yet

Wednesday’s rate cut and the likelihood of more to come is welcome news on the housing front, but how much it will stimulate homebuying remains an open question.

“There appears to be pent up demand in both the auto and real estate markets,” Texans Credit Union CFO Ben Hart told CandysDirt.com. “Consumers have been holding off on large purchases in anticipation of lower rates.”

Still, Hart said he doesn’t expect a big surge of homebuying in the Lone Star State after just one rate cut of 25 basis points.

“I think there’s going to have to be more cuts to really improve homebuying demand because of the way home prices have remained higher despite this higher interest rate environment,” he said. “I think a 100 basis point reduction in interest rates will need to be realized before we see a significant impact on mortgage demand.”

One of the checks on the market has actually been how great mortgage rates were for consumers in the immediate aftermath of the COVID-19 pandemic.

“A large portion of Americans got into homes when rates were at historic lows. There’s a reluctance to give up that 2-3% mortgage rate to upgrade their house,” Hart said. “That trend is pressing up against mortgage demand. We’re seeing that it’s often life events pushing existing homeowners to take out that new mortgage.”

With the median sale price in Texas coming in around $343,000 these days, the delivery of more housing stock is also sorely needed.

“Among first timers, we do see less reluctance [to enter the market] because those consumers don’t have low interest rates in the back of their mind as they’re exploring homeownership,” Hart said. “The challenge for those folks is low inventory in the entry level homes category.”

Mortgage rates went up afterward. The Fed is about short term yields and mortgages are long-term yields.