Richardson-Based Lender Gets Creative With First-Time Homebuyers Program

Share News:

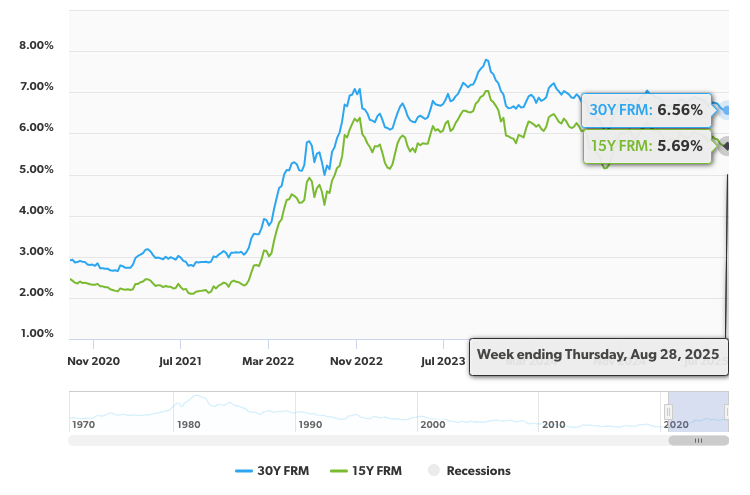

Between high interest rates and dizzying listing prices, the housing market’s been tough for first-time homebuyers to break into. Now, while the Federal Reserve might be coming to the rescue over the course of the next year or so, some lenders are getting creative with specialized products geared toward folks with limited liquidity.

Before diving into what’s out there, there’s something first-time homebuyers should get straight about entering the market. First of all, believe it or not, you don’t need to put anywhere near 20% down on a home. In fact, first-time homebuyers haven’t been dropping any more than 10% on average since the 1980s. Maybe if more Zoomers knew this, they wouldn’t be so pessimistic about their homeownership prospects.

Still, with home prices being what they are, even a small percentage down can mean at least several thousand dollars. The median sales price in July nationally was $422,400. Texans did better at $351,600. And then, of course, there’s still closing costs that need to be thrown in, and those can run anywhere from a couple grand to several thousand bucks.

Angie Jackson, vice president of real estate lending at Texans Credit Union, told CandysDirt.com that one of the most frequent issues raised by prospective first-time customers has been affordability, so she took the lead on developing a suite of products to help them out.

“We knew that we needed to design products that would enable an applicant to come to closing with little to no upfront dollars out of their pockets,” she said. “That was one of the most important things we learned we needed to be able to do.”

The program she developed includes three options that aim to address borrowers’ liquidity issues:

- Mortgages with as little as 3% down

- Flexible-rate loans structured so that initial payments are lower

- Financing with closing cost credits (up to 105% of the home’s value)

“We’ve crafted these innovative products in such a way that they, from a viability perspective, still held true to what the credit union’s goals were,” Jackson said.

Richardson-based Texans Credit Union got its start in 1953 as a financial cooperative for Texas Instruments employees. It’s since grown to service the whole of the Lone Star State.

Jackson said the non-profit lender has already seen a significant uptick in new inquiries regarding the first-time homebuyers program. She also shared an interesting fact, the definition of a first-time homebuyer is surprisingly broad under Federal Housing Administration rules.

“Most of the time, individuals believe that first-time homebuyer means it’s my very first time ever having homeownership rights. The true definition is that you have not had homeownership rights on any property within the last three years,” she said.

This covers both people who may have lost their previous home due to hardship (think foreclosures and short sales) and those who may have cashed in when the market was hot but are looking to become homeowners again.

While it might be some time before mortgage rates get back to a more comfortable 3-4% range, it’s not necessarily all doom and gloom out there for “first-time” homebuyers. There are financing options out there — and now Texans have three more.