New Short-Term Lending Platform for Home Flippers Has National Designs

Share News:

A Dallas-based short-term lending platform with serious money behind it is looking to scale up and become the go-to source of reliable financing for home flippers.

Crebrid (think credit and bridge, as in bridge loan) has gone all-in on leveraging AI to put itself at the forefront of fintech. The company previously operated out of Plano as Wildcat Lending, clocking about $2 billion in financing across 10 years in the fix-and-flip market before rebranding.

Tim Jordan, president of Crebrid, sat down with CandysDirt.com at the company’s offices in Preston Center. No stranger to real estate and finance, Jordan is also no stranger to Crebrid’s digs at 8343 Douglas Ave. He worked in the same suite when he was with JLL, before the firm moved to Uptown.

“I’m literally one office over from the office I was in for seven years,” he said. “It’s like coming back home for some of us that came over.”

He pointed over to a corner office that had been converted into a conference room. It used to be Roger Staubach’s office.

“We made it a conference room because I didn’t want anyone officing in Roger’s old office,” he said.

That sense of familiarity, however, isn’t slowing Jordan’s ambitions for his new company.

“Our goal is to make this a national business,” he said. “It’ll be based here, but we’re going to grow it nationally in key markets where we really like the trend of the market, where there’s good fundamental growth and activity.”

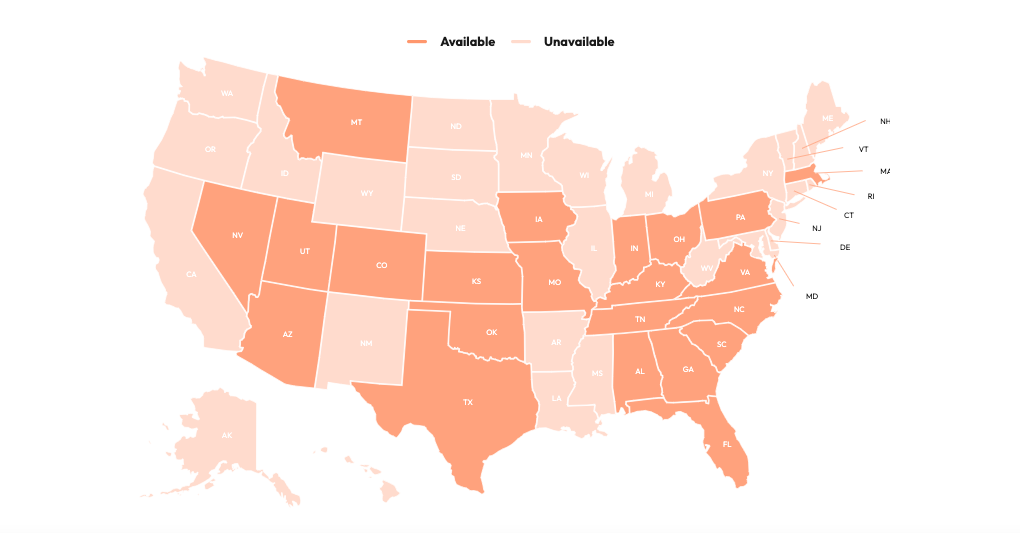

Jordan pointed to states like Colorado, North Carolina, South Carolina, and Utah — and of course there’s Texas, which he described as relatively lender-friendly. He said the platform is primed in 26 states so far.

The selling point for Crebrid is its deployment of technology to minimize manual processes and maximize accuracy when it comes to the collection of large sets of housing trend data.

“Our technology mitigates risk from the process,” Jordan said. “When every system is connected, you’re not re-keying the same data in different places, and that means fewer mistakes, faster decisions, and more confidence in the numbers.”

Humans will still be conducting analysis and making risk assessments, but the basic idea is to establish a speedy and user-friendly platform for those in need of short-term loans, namely house flippers, a demographic that’s currently being under served by traditional banking institutions.

Jordan said the platform takes just seconds to spit out a rate quote after the applicant inputs information about the property they’re looking to buy and their necessary personal and business information. It will also allow users to explore financing for multiple properties at once.

“The hoops that a bank has to go through to lend to anyone in housing, they would never do what we’re doing,” Jordan said.

House flippers typically have to rely on private lenders for capital, and they have to fix and resell before the value they add to a home (their profit) gets eaten up by the higher interest rates associated with short-term, hard money loans.

“That’s their living. You buy a $200,000 house, you put $50,000 in it, and you sell it for $320,000. You make $50,000-70,000 a house. They do five or six a year, and that’s how they make a living,” Jordan said. “There are a lot of people in that business.”

While banks typically look at an applicant’s credit history, debt-to-income ratio, and pay stubs when assessing whether to issue a mortgage, Crebrid has its own set of criteria: cash on hand, credit, and experience with home flipping.

Earlier this summer, the global investment management firm Barings committed $500 million in purchase facility, backing Crebrid in its plans to scale nationally.

“They would like us to do a billion this year, and then they want us to grow up to $2.5-3 billion over the next three to five years,” Jordan said.

He said Barings wanted to get behind the platform because its predecessor, Wildcat Lending, had a very low default rate.

“They were very good underwriters, very efficient underwriters. That coupled with the technology we’re pairing with it to help grow the business and automate a lot of things — that’s really the key to us being able to grow our footprint,” Jordan said.

CandysDirt.com asked Jordan about the possible ramifications of President Donald Trump’s tariff policy on the fix-and-flip market. While he acknowledged construction costs are a serious concern for builders, he said that home flippers are far less exposed since they’re primarily dealing with things like flooring, cabinetry, and interior design. He pointed to interest rates as the biggest obstacle, since they are directly affecting people’s housing choices, namely by limiting them.

Excellent article!