Republic Title Tip: Understanding Survey Deletion Coverage in Texas

Share News:

When navigating complex property transactions in Texas, having a trusted partner like Republic Title can make all the difference. Republic Title has long been recognized as a reliable resource for homeowners and real estate professionals, offering invaluable insights and solutions for various issues, including the critical aspect of survey deletion coverage. In this article, we will provide a comprehensive understanding of this essential component of title insurance.

What is Survey Deletion Coverage?

Survey deletion coverage, also known as survey coverage or survey amendment, covers any errors and omissions by a surveyor. This coverage provides assurance the survey of the property is accurate, that all improvements are accurately depicted, and that the property lines are properly defined.

Equally important — what survey coverage does not insure. Survey coverage does not insure against matters, conflicts, discrepancies, or encroachments that are shown on the survey.

In a standard title policy there is an exception for “any discrepancies, conflicts, shortages in area or boundary lines, or any encroachments or protrusions, or any overlapping of improvements.” When survey coverage is purchased, the exception is revised to read only “shortages in area” which provides the insured with significant additional coverage, as explained below.

What is Required to Obtain Survey Coverage?

To obtain survey deletion coverage in Texas, you typically need the following:

a. A current survey that accurately reflects the property lines, improvements, any easements, setback lines, or other items that are located on the property. If the Seller in a transaction has an existing survey it may be possible to use the survey as long as there have not been any changes to the property since the survey was prepared. If the Seller has an existing survey be sure to check the appropriate boxes in Paragraph 6 of the TREC 1-4 Family Contract (the “TREC contract”) and deliver the survey and the T-47 to the Buyer and Title Company within the number of days stated in the contract. The survey will be reviewed by the Title Company and must meet certain criteria and standards to be accepted. If an existing survey is not acceptable to the title company a new survey will be required, and the party responsible for that is negotiable and is set out in paragraph 6C(1) of the TREC Contract.

b. A new survey may be required in certain circumstances. If the Seller does not have a survey, if they have made changes to the property since the last survey was done, or if an existing survey is not acceptable to the Title Company, a new survey would have to be ordered. The party responsible for paying for the new survey is negotiable, and is set out in Paragraph 6C of the TREC Contract. It is important to note that a new survey cannot be prepared until the title work has been completed, so keep that in mind when calculating the number of days the parties have in Paragraph 6 to provide the new survey.

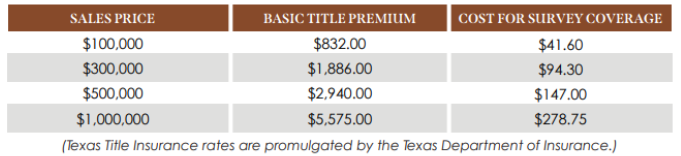

c. Request Survey Deletion Coverage: This is typically requested by checking the appropriate box in Paragraph 6A(8)of the TREC. The party who will be responsible for paying the premium for survey coverage is negotiable and can be set out in Paragraph 6A(8)(ii). The cost for survey coverage on a residential transaction is 5 percent of the basic premium. See the chart below for some examples of the cost:

Even with survey coverage, it is important to note that a Title Company will add any necessary exceptions for items disclosed on the survey thereby removing those items from coverage in the title policy even when survey coverage is provided. For example, if the survey shows that a fence encroaches on to the neighbor’s property, the Title Company will revise the title commitment to add an exception. The Buyer would have an opportunity under the TREC Contract to object to the new exception under Paragraph 6D of the TREC Contract. If no objection is made, and the Buyer purchases the property, and a dispute arises regarding the fence, it would not be covered under the Title Policy.

Why is the Phrase “Shortages in Area” Not Deleted from the General Exception?

One notable aspect of survey deletion coverage in Texas is that the phrase “Shortages in Area” is not deleted from the general exception. This phrase is included in standard title insurance policies, and it signifies that the Texas Department of Insurance prohibits title companies from insuring exact acreage. In other words, the title insurance policy does not provide coverage for discrepancies in the property’s area or size.

The reason for not deleting this phrase is to take into account the fact that Surveyors and Appraisers may use slightly different methods and technologies to measure property area, and discrepancies can arise. By retaining the “Shortages in Area” phrase, it clarifies that the title insurance policy does not guarantee the property’s exact size, only the boundaries and encroachments.

What is the Benefit of Purchasing Survey Coverage?

The primary benefit of purchasing survey coverage is protection against unexpected boundary issues and encroachments. Here are some key advantages:

a. Legal Protection: Survey coverage offers legal and financial protection in case a dispute arises regarding the property’s boundaries or improvements. For example, if someone claims ownership of a portion of your land or that they have a right to use a portion of your land, the title insurance company will step in to defend your rights and potentially cover any financial losses.

b. Potential Cost Savings: In the event of a boundary dispute involving a matter covered in your title policy, the title insurance company may be required to cover legal expenses and potential settlements, saving you from bearing these costs yourself.

Why Should You Not Use Old Surveys When Buying a New Home?

Using old surveys when buying a new home can be risky for several reasons:

a. Changes Over Time: Property boundaries and improvements can change over time due to various factors, including renovations, construction of new structures, installation of new fences along a boundary line, or land erosion. An old survey may not accurately reflect these changes.

b. Encroachments: An old survey may not identify encroachments from neighboring properties or other issues that have developed since the survey was conducted. This could lead to boundary disputes and costly legal proceedings.

c. Title Insurance Requirements: Most title insurance companies require a current survey to provide survey deletion coverage. Using an old survey may result in the denial of coverage or additional costs to update the survey.

d. Lender Requirements: If you are obtaining a mortgage loan to purchase the property, your lender may also require a current survey to ensure the property’s boundaries, easements, and setback lines are accurately defined.

In Texas, survey deletion coverage is a crucial aspect of title insurance that can protect homeowners in certain property disputes and from financial losses related to property boundaries and improvements. Republic Title’s commitment to serving as a trusted resource for homeowners and real estate professionals is evident in its expertise and dedication to secure property transactions in Texas.