The 2-1 Buydown: Are They Worth The Trouble to Attract The Right Buyer?

Share News:

Welcome to this week’s Tarrant County Tuesday edition, where we delve into the intricacies of real estate financing. Today, we’re spotlighting a financial strategy that’s been gaining traction in the housing market — the 2-1 Buydown.

First of all please keep in mind that I’m a bow tie-wearing real estate sales professional by day and a long time ago I went to a little public university in the Austin area, so I don’t do math and numbers. Therefore I have reached out to two local lenders I value, respect, and have worked with for nearly two decades — Gary Linville of Legacy Mutual Mortgage and Bailey Head of USA Mortgage — for their input on buydowns.

What is a 2-1 Buydown?

The 2-1 Buydown is a compelling mortgage option that empowers both buyers and sellers. It offers an attractive incentive for potential homeowners, making it easier to afford their dream home. In this era of increasing interest rates and relentlessly high housing prices, the 2-1 Buydown is becoming more and more popular.

“The 2-1 Buydown helps the buyer with a much lower payment than is current market, then increases after year one and then increases one more time the following year,” explains Linville. “It allows new buyer to ‘grow’ into the house payment.”

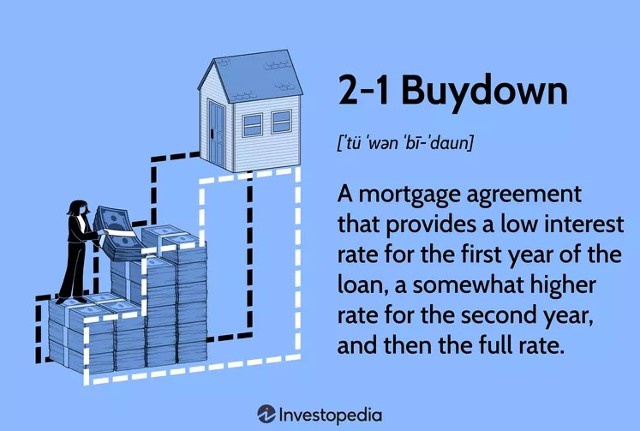

The 2-1 Buydown is a temporary interest rate subsidy provided by the seller, typically for the initial years of a mortgage. It’s structured as a temporary reduction of the interest rate during the early years of the loan, which then gradually increases over time until it reaches a stable level.

During the first year, the interest rate is reduced by 2 percent, followed by a 1 percent reduction in the second year. Subsequently, from the third year onwards, the interest rate stabilizes at its standard rate for the remaining loan term.

In today’s real estate world, the hope is that surely in two to three years the Federal Reserve will stop manipulating the interest rate and buying power of eager home buyers and interest rates will “settle” somewhere in the 5 to 5.5 percent range. If that’s the case, homeowners can easily refinance their 2-1 Buydown for a fixed rate that should be lower than when they first purchased their home.

Benefits for Buyers

What are some of the immediate benefits for buyers when it comes to a 2-1 buydown?

- Affordability: The initial lower interest rates during the early years of the mortgage make homeownership more affordable, enabling buyers to qualify for a higher loan amount and potentially a more desirable property.

- Transitioning Period: A buydown provides a smooth transition for buyers who may expect an increase in their income over the years. The graduated interest rate allows for gradual adjustments to higher payments.

- Financial Planning: Buyers can plan their finances accordingly, knowing that their monthly payments will increase incrementally after the initial years, helping them to budget wisely and effectively.

Benefits for Sellers

“Rather than reduce the price of the house, the seller can pay to reduce the buyer’s payment,” says Linville.

What are other benefits for sellers when it comes to a buydown?

- Market Attractiveness: Offering a 2-1 Buydown can a property more appealing to potential buyers, hopefully leading to a faster sale … or just a sale!!

- Competitive Advantage: Sellers can gain a competitive edge by showcasing this attractive financing option, especially in a competitive real estate market.

- Negotiation Power: A buydown can be used as a negotiation tool, giving sellers more flexibility in negotiations with prospective buyers

The goal of a builder or seller is to move the product. While some sellers might feel they are “showing all their cards ahead of a contract offer,” I would contend that buyers and their agents know where the power lies in October 2023 until inventory significantly increases or interest rates significantly decrease.

Sellers have very little negotiating power these days. Even when offering a buydown, a buyer will take that and still ask for for reduction in the contract price. Hey sellers, you had it great — no, BEYOND GREAT for the past handful of years. Do you think buyers aren’t licking their chops to inflict a little payback on you and others? If your goal is to sell your home and move on, time to take your medicine.

Things to Consider With a Buydown

“Buying down the interest rate with discount points is often a more attractive option than opting for a buy down,” explains Head. “It provides a straightforward and cost-effective way to lower your long-term borrowing costs. This approach allows you to enjoy lower monthly payments and potentially save a substantial amount of money in interest over the loan term.”

While buyers would certainly love the seller to pay for their interest rate to be lowered for the life of the loan, there are definitely increased costs involved in that scenario. Many sellers can’t or won’t pay that much money. Most buyers seem to know the interest rate has to, or will, decrease in a few years and are okay with the temporary buydown rate.

Other things to consider:

- Long-Term Planning: Buyers should carefully evaluate their long-term financial situation and ensure they will be able to afford the mortgage once the interest rates increase.

- Consult a Professional: Always, always, always talk to local lending professionals to fully understand the implications and benefits of the 2-1 Buydown.

“Ultimately the decision between the two comes down to how long they think they will keep the mortgage,” says Linville.

Final Thoughts on a 2-1 Buydown

In conclusion, the 2-1 Buydown is a financing strategy that merits consideration for both homebuyers and sellers in Tarrant County. Its ability to enhance affordability and market appeal makes it an option worth exploring in the vibrant real estate landscape of our county. As always, informed decisions lead to successful transactions in the real estate world.

they took out the Chevy Chase clip! What? Was greatness!