Four United Development Fund Execs Charged by Feds For Alleged Years-Long Ponzi Scheme

Share News:

- Two of the Indicted are Highland Park Residents

- Kyle Bass Takes to Twitter For Vindication

Prosecutors in the Northern District of Texas have taken definitive action against four executives with United Development Funding, the Grapevine-based real estate investment trust the FBI raided in February of 2016.

Two of the four are Highland Park residents who reside just south of Beverly Drive in a $6 million home. Agents involved in the sale say the home was purchased shortly before the raid.

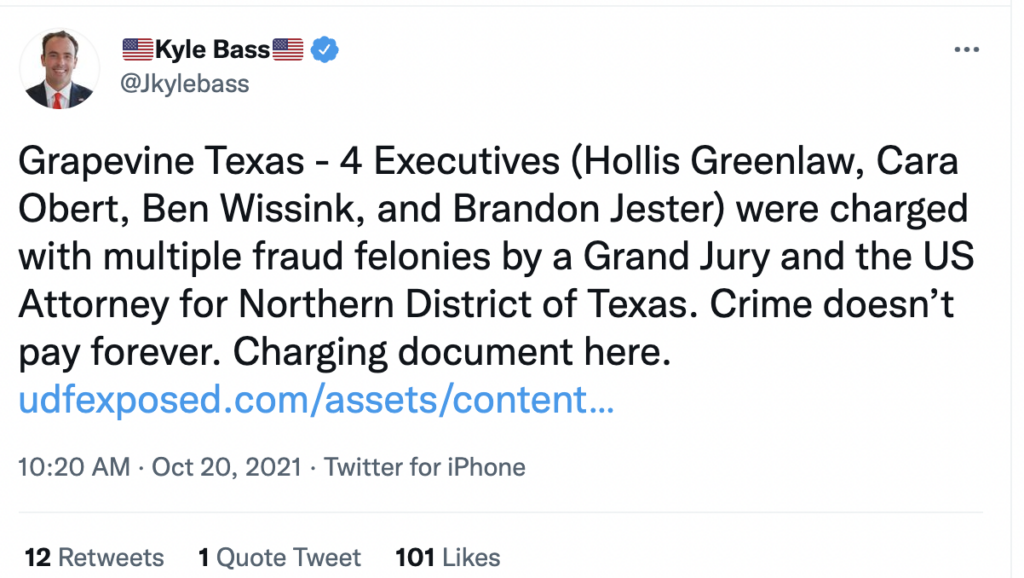

More than five years after that initial raid, the U.S. Attorneys’ office charged the four — CEO Hollis Greenlaw and three of his colleagues at the Grapevine-based real estate investment trust — with conspiring to deceive banks and investors through a series of real estate investment funds.

The defendants are Greenlaw of Colleyville, Benjamin Wissink and Cara Obert of Highland Park, and Jeffrey Brandon Jester of Wylie.

Greenlaw is a former Washington tax attorney with a degree from Columbia University School of Law and an undergraduate from Bowdoin University who once worked as a partner of The Hartnett Group, Ltd.

According to public records, Greenlaw and his wife, Angela, bought their Colleyville home in 2004. Greenlaw also sold a home in Vaquero shortly after the raid on UDF.

Wissink and Obert live together on Miramar in Highland Park, in a $6 million dollar home. Jester lives in Wylie.

The case is as complex as it long-winded, but it boils down to why this firm and these execs would jeopardize lucrative careers — if they did — and for what gain? It is made more interesting by the almost obsessive drive of a maverick Dallas fund manager who has relentlessly spent more than five years on a public relations campaign as well as intense legal fees to prove that UDF was defrauding investors.

The Fed’s charge is illegally commingling investment dollars from three of the firm’s different investment funds. But that, say some, is putting it mildly.

Prosecutors claim the four conspired to conceal the true performance of the fund’s business and its financial condition to stimulate investment and to enrich themselves. Greenlaw and other UDF managers defrauded investors and banks, they claim, by failing to disclose that shareholder funds were being used to repay developer loans and issue distributions to earlier investors, according to the indictment.

Here’s how Bloomberg puts it:

A 10-count indictment that dropped Oct. 15, first reported by Bloomberg Law, says that from 2011 through 2015, the four defendants (Greenlaw, UDF partnership president and committee member Benjamin Lee Wissink, UDF CFO Cara Delin Obert, and UDF director of asset management Jeffrey Brandon Jester) “did knowingly execute and attempt to execute a scheme to defraud the investing public and shareholders” by obtaining “money and property by means of materially false and fraudulent pretenses.”

Alleged: A Complex Scheme

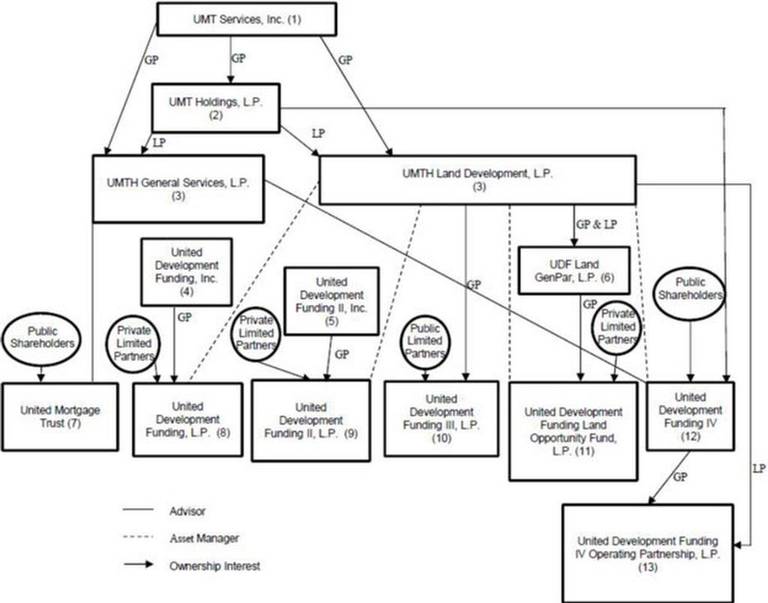

It’s a complicated scheme that almost requires diagrams on a white board to trace.

The defendants at UDF, say the Feds, packaged, marketed, and sold real estate investment packages to investors promising hefty returns of 8 to 9.57 percent. Investors were told the returns would come from the financing of land and real estate developments, of which there have been hundreds in North Texas over the last ten years: DFW is one of the fastest-growing areas of the nation. Of course, most REITS usually finance tangible assets, such as shopping centers, hotels, apartment and office buildings. But UDF loaned more than one billion to residential developers, according to the Fort Worth Star-Telegram:

Over more than a decade, UDF has made more than $1 billion in secured loans to residential developers under the guidance of CEO Hollis Greenlaw. It is organized in a web of more than a dozen corporate entities, with UDF IV fund as its only publicly traded unit.

To pay investors dividends they were due, the Feds say the defendants created another investment fund, repeated the promises, and paid the first investors from the new fund. This continued in a Ponzi-like scheme until Fund V.

The defendants are also accused of borrowing money from several banks whose assets are guaranteed by the FDIC.

According to the indictment, the defendants lied to the banks as to the purpose of the loans they procured.

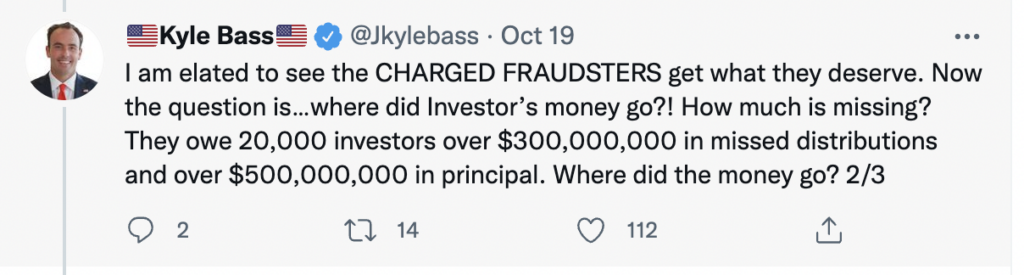

“They stole the savings of 20,000 people,” says Dallas-based hedge fund manager Kyle Bass. “Mom and pop investors, I have spoken to some of them. No one knows how much money is actually missing.”

Bass says the defendants raised a total of $1 billion over five funds, with no audited financial statements to account for the money.

Bass has been drilling down on UDF since 2015, when he made the unprecedented move of forming a website and publicity network expressly to accused UDF of wrongdoing in public. He did so after one of his analysts, Parker Lewis, found high dividends and undisclosed accounting discrepancies:

After months of research, he locked onto an explanation: When borrowers struggled to repay their loans, UDF used cash raised by newer funds to pay investors in older ones. Sometimes the newer funds would buy pieces of loans owned by the older ones in an effort to ensure that cash was available. These actions allowed UDF to keep paying the sizable dividends investors had grown to expect, which meant that it could continue attracting new investments.

UDF was operating a Ponzi-like scheme, said Parker, which raised a red flag signaling major losses for investors. As for his motive, Bass wanted to protect investors like the ones he has met, including a man who worked for 40 plus years at Bell Helicopter and then invested in the funds to secure his retirement.

The public damning by Bass and Hayman got the media’s attention, and led to multiple civil lawsuits against UDF by shareholders. UDF also disclosed it had been the subject of a “fact-finding” investigation by the SEC since 2014, making it clear the SEC said the investigation was “not an indication of any violations of law” and said it had not been accused of any wrongdoing.

The “fact-finding” ended in 2018, when the SEC sued UDF and five of its senior executives, including Greenlaw, Obert and Wissink, for violating several SEC rules. The execs paid about $8.2 million in fines but denied no wrong-doing. The company was spared the fines.

Speaking of fines, one of UDF’s auditors, Whitely Penn LLP, was sanctioned by the Public Company Accounting Oversight Board (PCAOB): $200,000 for violations of “PCAOB rules and standards” in connection with UDF audits and financial statements.

UDF retaliated by suing Bass and Hayman Capital for business disparagement and tortious interference, as well as orchestrating to profit from shorting UDF stock. (Bass and Hayman did short the stocks.) Bass and Hayman are well-known for short-selling, an old investment tactic utilized by hedge funds and others to profit off a company’s declining stock assets by betting on them. While most of us buy low to sell high, shorters sell high to buy low. Shorting is seen by some as a way to keep companies on their toes and honest, while critics say they manipulate markets.

“Traders bet against the first public company, the Dutch East India Company, 400 years ago.”

Case Status

The UDF lawsuit against Bass and Hayman is in discovery with a trial set for May of 2022. Recently a mandamus was granted to Bass that found error in a lower court’s ruling over certain confidential documents. Jeff Tillotson is now lead counsel for Bass and Hayman.

“We believe strongly that evidence is going to show that postings by Mr. Bass were not only completely accurate, but the facts are much worse,” says Tillotson. “Mr. Bass views it as further vindication that his initial review and assessment is now confirmed by the authorities.”

Bass has earned credibility in real estate by being one of the few investors that saw the subprime mortgage crisis coming: he bet against subprime mortgages in 2007, he and his investors profited handsomely. Subprime mortgages — remember The Big Short? — were the catalyst for the massive 2008 financial crisis that led to the largest U.S. recession since the Great Depression.

As they have for six years, UDF lawyer Paul Pelletier vehemently denies the charges and says the government is over-reaching. All defendant’s plead not guilty on their first court appearance in Tarrant County last Friday, October 15. Bass says the four were fingerprinted and booked on Tuesday. The trial begins December 6 in Fort Worth.

“For the past 6½ years UDF has endured an illegal predatory short and distort attack, an unlawful FBI search and a transitory government investigation with ever-changing theories of alleged liability,” Pelletier (Paul Pelletier) said in a statement.

But Bass says more is yet to come:

Kyle Bass nails it again!

What a crazy journey to this point. Needless to say, we’ll be watching what happens.