Is the North Texas Real Estate Market Sputtering? More Like a Soft Landing?

Share News:

Huge Wall Street Journal story being circulated via Twitter, etc. today, “The U.S. Housing Boom Is Coming to an End, Starting in Dallas.”

Dallas, really?

“Home prices zoomed higher in recent years, and mortgage rates are climbing. Buyers are queasy.”

PLANO, Texas—A half-hour drive straight north from downtown Dallas sits one of the fastest-growing counties in the country. Cotton fields have been replaced with Toyota’s new North American headquarters, a Dallas Cowboys training facility and a sand-colored shopping strip with a Tesla dealership and a three-story food hall.

Yet even with the booming growth, Dallas’s once vibrant housing market is sputtering. In the high-end subdivisions in the suburb of Frisco, builders are cutting prices on new homes by up to $150,000. On one street alone, $4 million of new homes sat empty on a visit earlier this month. Some home builders are so desperate to attract interest they are offering agents the chance to win Louis Vuitton handbags or Super Bowl tickets with round-trip airfare, if their clients buy a home. Yet fresh-baked cookies sit uneaten at sparsely attended open houses.

First of all, developers have long offered agents perks to sell their homes — hate to tell you, but Louis Vuitton handbag lures are nothing new. (I sure hope they are not knock-offs!) We have talked before about the North Texas slow down, particularly in million dollar plus homes.

How many ways can an agent say “price reduced” without really saying it?

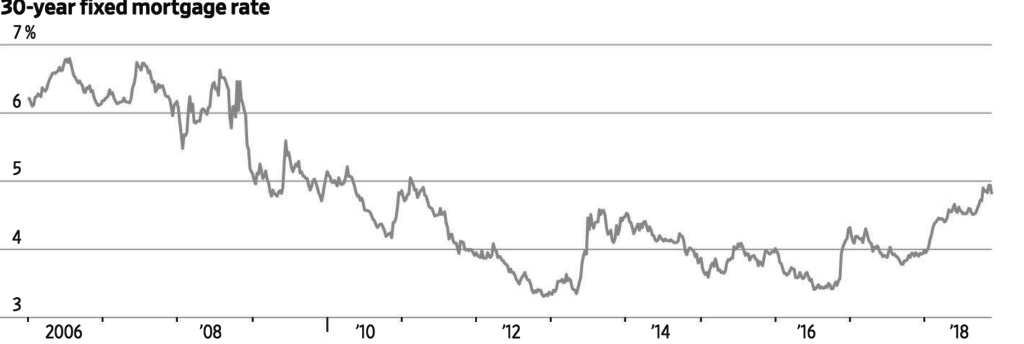

It’s a classic economic cycle story: inventory contracts, demand expands, so home prices go up up up almost beyond reason, where I think we have been quite recently. Nail in coffin: this year interest rates started to creep upwards, combined with major changes in the tax code. I have heard my share of experts say that the changes in home mortgage and property tax deductibility will not affect buyers, but you know what?

I think it will. When you pay upwards of $20,000 a year in property taxes which are no longer 100% deductible, you start thinking of what else you can do with that money. Plus North Texas home prices have risen faster than our wages even though we got like 100,000 jobs a year over the last five years. We got those jobs BECAUSE of lower wages:

Dallas, which had the second-strongest annual increase in employment of any metropolitan area in the country in September, helps explain why. Even though the economy in the sprawling metro area has boomed, home prices have grown much faster than wages, and buyers have been straining to afford homes.

“I agree with most of the article” says veteran appraiser DW Skelton. “But I don’t like the example of Plano. There is not that much inventory left in Plano for land development, hasn’t been for years. Developers are really going north to Frisco, Celina, McKinney and beyond, or west to Colleyville and Grapevine, where there is still land to develop.”

But at least, says DW, we are not seeing developers give away luxury cars, at least not yet.

So “sputter”? DW calls the current market conditions more of a “soft landing”, something he has long heard of, but never seen.

“It’s moving down to Preston Hollow without a doubt,” he says. “Housing prices just got too high. A couple of years ago it was difficult to even appraise properties, a lot of us going on “opinion of value”. We have heard about this soft landing since I’ve been in the business. But I have ever seen it start filtering down to a reasonable level.”

DW actually thinks a little break in the market may be a good thing. We are certainly nowhere near the Death Star days of the mid-80’s when Fannie Mae bulldozed entire home developments until the recession was over because it was cheaper to maintain raw land than empty houses.

“Those were the days of “jingle mail: if the envelope jingled because it had keys in it, they were sending the keys back in to the bank,” recalls DW. “If we get lucky, we’ll have a a soft landing.”

If not, I guess we will crash and the rest of the country will follow.

Dallas has been the “canary in the mine shaft” this housing cycle, said Paige Shipp, regional director for Metrostudy, a consultant to home builders. Homes are taking longer to sell, bidding wars are rarer and price cuts are more common as buyers absorb the impact of higher rates.

That’s because more Dallas residents rely on mortgages than folks in other parts of the U.S. do, such as bonus-rich Silicon Valley. While cash buyers and large down payments are common in booming West Coast markets, the average household in Dallas finances 83% of its home purchase.

That figure is only slightly higher than the national average of 81%, according to Black Knight Inc., a mortgage data company. In San Francisco and Seattle, buyers on average finance 74% and 79% respectively.

When the bank owns most of your home, giving it back is not all that hard.

But what about jobs? What about inventory. Are we also overbuilt on apartments? To be continued…

I don’t disagree with this article at all – I don’t think this is sustainable and frankly terrifying. I’d like to see that 235k home that doesn’t need to be torn down or extensively remodeled. I live in what I considered the last affordable neighborhood in Dallas (sw corner of lovers & Inwood) in 2014 we purchased our 2/1 for 205K and put some money in for a new kitchen and bathroom, we’re still under 300K – the modular home across from me sold for 300K and was torn down. So now the land value is 300k, not even the structure. A new home three doors down was just sold for 1mill+ that’s all fine and dandy for the value of my home, but sadly we are now priced out of our own neighborhood if we ever wanted something bigger in the same area. We both have decent paying jobs but there is no way our salaries have kept up with housing costs. It’s sad to think my next step for a bigger home would be north, WAY north of 635. Not. Happening. Ever.

Thanks Tina, you are exactly the demographic this article was aiming at! These sky-high home values only help when you sell, and inflate property taxes.

I think one area to watch is the potential overbuilding of luxury multi-family, especially the sheer number of apartment towers where $3-4 per square foot is not uncommon. Time will tell.

Will the under $200k market increase its inventory at some point?