Texas’ SB 2 Property Tax Reform Bill A Good Start But Benefits Wealthy More Than Others

Share News:

On November 29 I read a story in the Fort Worth Star-Telegram about a bill before the Texas Legislature (SB 2) to stanch the tax increases felt across the state by homeowners. I decided to read further and downloaded the 90-page interim report by the Senate Select Committee on Property Tax Reform & Relief that’s the impetus behind the SB 2 bill mentioned by the Star-Telegram.

Gosh, but property taxation in Texas is a huge CF.

I’ll begin with the flaming pink elephant in the room: Nowhere does this report recommend or even acknowledge that non-disclosure of real estate transaction sales prices is a big part of the problem. As I’ve written ad nauseum, without accurate data on actual property sale prices, no Central Appraisal District (CAD) can make the most accurate valuations of property. I say this system favors the wealthy because lower-priced properties are appraised with more accuracy. Looking as I do at multi-million dollar properties for sale in Dallas, I can tell you it’s the RARE property that’s actually appraised at anything near its asking price. I can also tell you it’s overwhelmingly these same people who hire tax consultants to plead their case with the CAD for lower valuations at the same time their home is listed for millions more than the assessed value. It’s such a time-worn tactic of the wealthy, it’s even presidential.

That said, the system is also opaque, seemingly by design.

First, there are two components that factor into your property tax bill. There’s the assessed value derived by the CAD using some witch doctor formula and then there’s the rate of taxation. Both can be protested, but at a cost.

The report noted that, “Despite the fact that taxpayers know they can protest the appraised value set by the CAD to their ARB [Appraisal Review Board], testimony was repetitive that the state’s property tax system is unfair to taxpayers. Taxpayers know they have a right to be heard, but their testimony indicated they do not expect to be treated fairly by the ARB.” (I’ll add my own “true dat.”)

The report also cited instances where CADs kept blacklists of ARB members (members of the public) to disinvite the following year because they were viewed as too soft on giving homeowners a break. Gee, I can’t understand why homeowners feel the system is rigged …

As for the taxation rate, in addition to schools and such, there are two components. Maintenance and Operations (M&O) does what it says, it’s the kitty that maintains the city’s day-to-day expenses. Then there’s the Interest & Sinking (I&S) component that is used to repay debt from bonds and the like. I&S is fairly fixed, moving with bond interest rates, while M&O can be rolled back if it exceeds 8 percent revenue growth annually (known as the rollback rate). Eight percent may not seem like a lot, but remember that it’s a CAD-wide number, not an individual property, which for a homesteader can go up 10 percent a year. Plus, a CAD can be at 7.99 percent forever and cumulatively, that adds up (as we in Dallas know). Interestingly, new construction and first-time homestead exemptions are excluded when calculating the rollback rate. In development-happy Dallas, actual tax revenue increases can be (are) much higher than 8 percent.

For Dallas readers, the report gives this example, “For example, the city of Dallas and Dallas County have left their tax rates static from 2012 to 2015. The city tax rate has remained at 79.7 cents per $100 of property value and the county has left the rate at 24.31 cents per $100 of property value. Back in 2012, both the city and county rates were several cents under the rollback rate. But now, as property values have risen, both Dallas County and the city of Dallas are now taxing within less than half a cent of the 8% rollback rate. Over the same span, property values have risen by more than 19% in both taxing units. Because of this value increase and the lack of reduction in either entity’s rate, taxpayers are paying over 19% more in taxes in 2015 than they were in 2012.” (Or 35 percent more if you’re me.)

For those in Tarrant County, take solace in knowing that according to SB 2 author State Sen. Paul Bettencourt, R-Houston, “Tarrant County is the number one, most complained about county in the state,”

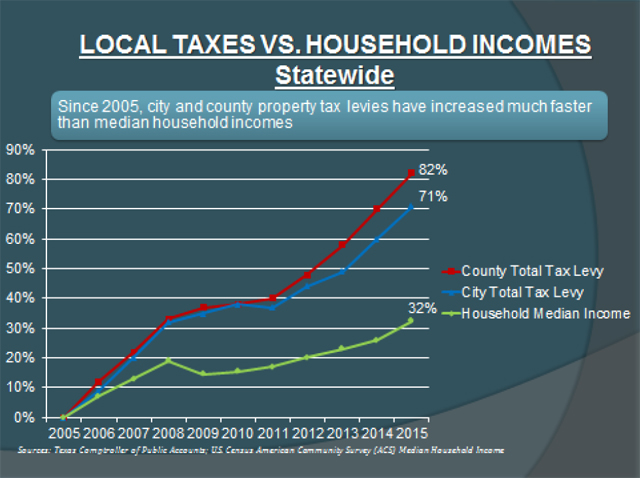

In Bexar County (San Antonio), they’ve, “seen a 30% increase for three years in total revenue” derived from property taxes. In fact, in Texas’ largest cities, property taxes paid rose 2.5-3 times the rate of household income growth since 2005. This gets at the heart of my tax ideology.

When you look at public opinion on taxes, decades ago people were more OK with much higher tax rates than exist today. Why? Because the higher rates were a smaller impact on overall buying power. With stagnant wages going back decades coupled with cost of living increases, taxes eat disproportionately into spending power. Had wages even kept pace with inflation, public opinion, I predict, would be vastly different on the subject of taxes. Think about it. Had your household income doubled or tripled since 2005, would you be crying as loudly about your tax bill? Doubtful.

This duality of tax rates and appraised values offers many finger-pointing opportunities. City leaders can crow they’ve not raised the tax rates (they’ve not) as they bask in their newfound wealth. CADs can say they’re just doing their job of appraising property (with whatever Ouija board they use) and not raising taxes either. And yet the pot of money grows.

But yes, as I said, citizens can, as a group, protest the tax rates but only after the 8 percent rollback is triggered. And even then, 7 percent of registered voters would have to sign a petition within 90 days to trigger a rollback election. Not enough signatures, no election and the higher rate is adopted. Because of this, protesting rate increases is difficult at best. One of the core tenants of SB 2 is to lower the rollback rate to 4 percent and then it would automatically trigger an election (like school tax votes).

But even then, there are ways to cheat the system. The report held Galveston County as an example of poorly scheduling votes on school taxes. Of the five scheduled from 2008 to 2016, voter turnout ranged from 4-11 percent. None were scheduled to coincide with major national or state election dates. All five school tax increases were passed based on startlingly little voter participation. One was even scheduled days before Labor Day. No shock that it garnered the lowest turnout of four percent. One might argue this constitutes voter suppression.

And it gets worse.

These special votes on school or property taxes are not required to follow the same rules as other “real” elections. For example, they do not have to use county administrators to run the election, nor must they comply with requirements for polling stations and electronic voting machines. One Houston MUD election was held in a residential garage while some in Plano said some school districts used “rolling voting” whereby the polling location moved throughout the day to locations where voters favoring the tax were located.

Further, general elections require 78 days to prepare the necessary balloting for absentee voters. Because tax ratification elections only need 30 or 45 days, it’s less likely absentee voters will be able to vote. Short windows also equate to less time to publicize the vote.

SB 2 wants all such votes to be held in concert with national or statewide elections in November. Seems pretty straight-forward and obvious to me. It’ll be telling to see which CADs whine the most (likely the ones with the most to gain from the current system).

Back to the flaming pink elephant of real estate purchase price disclosures. Were CADs to have access to real sales data and actually appraised property at its true value, not only would the wealthy have to pay their fair share, but the resulting tax revenue increases would blow the lid off the 8 percent rollback rate and force an election on tax rates across the state. And I guarantee the Texas Legislature and cities across Texas would fix those whopping big bills before they came due because if they didn’t, they’d all be out of a job come election day.

And that’s why accurate data matters. SB 2 makes sense, but it lacks one very important, flaming pink component.

Remember: High-rises, HOAs and renovation are my beat. But I also appreciate modern and historical architecture balanced against the YIMBY movement. If you’re interested in hosting a Candysdirt.com Staff Meeting event, I’m your guy. In 2016, my writing was recognized with Bronze and Silver awards from the National Association of Real Estate Editors. Have a story to tell or a marriage proposal to make? Shoot me an email [email protected].

the biggest issue I have with single family property tax assessments is the fact that a property is valued based on surrounding sales. If I don’t sell my property, how can it be valued higher (or lower)? Property should only be revalued at sale time, because that is the only way to accurately value something. Furthermore, I absolutely resent my local appraisal district raising my rates just because I choose to pave my rural driveway with concrete instead of leaving it a washed out, rut filled mess. The only time something like that could raise the value is when it is sold.

California tried this with Prop 13 and while property owners like it, it placed a huge hole in state budgets. And like any government budget hole, it was recouped elsewhere. In Texas, without a state income tax, it would likely be an increase to sales tax which would unfairly burden non-homeowners and the poor.