Debbie Downer: Today is QM and ATR Day, and Mortgage Brokers Say We Won’t Be Happy

Share News:

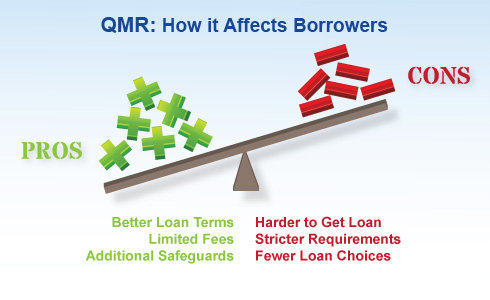

QM is not the Queen Mother, it’s Qualified Mortgage and Ability to Repay, fed monetary policies that start January 10. Mortgage brokers say we won’t like these new rules and they are going to put a crimp in real estate sales.

QM is not the Queen Mother, it’s Qualified Mortgage and Ability to Repay, fed monetary policies that start January 10. Mortgage brokers say we won’t like these new rules and they are going to put a crimp in real estate sales.

“The rules were cut and pasted from the HUD handbook that was written in the 1940’s, haven’t been updated since the 1990’s and were designed for low income borrowers in mind,” says Scott Drescher with Supreme Lending.

But they apply to everybody.

“They were not updated in any way. Worse, they do not reflect mortgage reality outside of FHA underwriting guidelines. Therefore, they’re not good for anybody as iron-clad rules.”

The changes that take place today will negatively impact the following business segments, according to Scott: buyers, sellers, borrowers, Realtors, builders, contractors to builders, appraisers, surveyors, title companies, home remodelers who rely on new sales or refinances, construction materials companies and retailers, cities that get income from new construction fees, and, oh yeah, mortgage companies, plus the trickle down industries.

This will, however, positively impact attorneys, compliance companies, and (he says) that is all.

This will, however, positively impact attorneys, compliance companies, and (he says) that is all.

Two sets of guidelines will exclude borrowers who are not necessarily high risk and would have paid the mortgage in full and on time. But they will increase the time and costs for lenders to process loans, which means that borrowers who are lucky enough to qualify will pay more. They will also disqualify some borrowers after they were pre-approved, appraisals were done, even after an initial underwriting approval, as the final analysis may throw the loan into a class that the lender cannot approve.

You think you deserve a loan because you have great credit and decent income? The government is not so sure.

The Consumer Financial Protection Board is fond of saying that lenders are allowed to do non-QM loans, even to the point of encouraging them. The problem is that lenders cannot, in most cases, afford to take the risk because the cost for failure is so incredibly high compared to the income from a loan that succeeds.

Look at this: the net profit from a closed loan of $200,000, a starter home, might be $500. The cost for a single failed non-QM loan of $200,000 could easily top $300,000 even if there is no intentional misdeed involved.

+$500 versus -$300,000… that’s easy math.

What do you think is going to happen to our market after today’s implementation? Have you had any “fun” with loans falling through on the eve of closing? It’s Friday — time for Debbie Downer!

Good job, Candy.

Thanks Harold! How are you? Miss you guys!