Don’t Hold Your Breath for Relief on the Mortgage Rate Front

Share News:

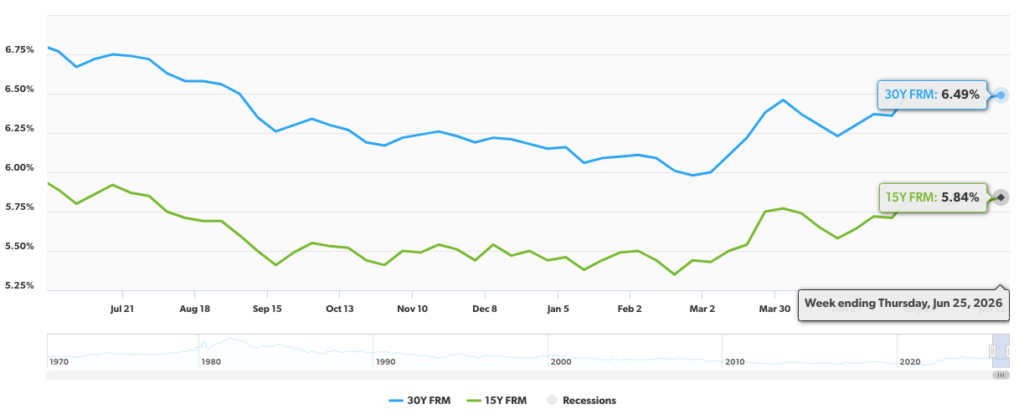

It’s been a minute since we checked in on mortgage rates, and there has been no shortage of heartburn in recent months. The downward trajectory of 2025 gave way to the inflationary pressures and economic uncertainty wrought by the war in Iran, dashing the hopes of homebuyers who thought better rates were on the way.

As of the week ending on June 25, the 30-year was clocked at 6.49%, according to Freddie Mac. That’s nearly half a point on the wrong side of the psychologically important 6% rate that would enable some several million would-be homebuyers to afford a median-priced home.

For the first time in three years, the 30-year hovered right at or just below 6%. Borrowers enjoyed those rates for a couple of weeks in late February before the war in Iran triggered an energy crunch and its cascading effects across the global economy.

In May, Kevin Warsh was sworn in as the new Federal Reserve chair, replacing Jerome Powell. President Donald Trump had nominated Warsh with the expectation that the Fed would move toward a looser monetary policy. But in the Fed’s first meeting with Warsh at the helm earlier this month, the central bank left its benchmark interest rate unchanged at 3.5% to 3.75%, signaling that persistent inflation remains a greater concern than relief for borrowers.

Mortgage rates aren’t directly tied to the Fed’s benchmark, but they tend to follow the trajectory. At this month’s Fed meeting, the central bank signaled there could be a rate hike later this year — probably not what prospective homebuyers wanted to hear.

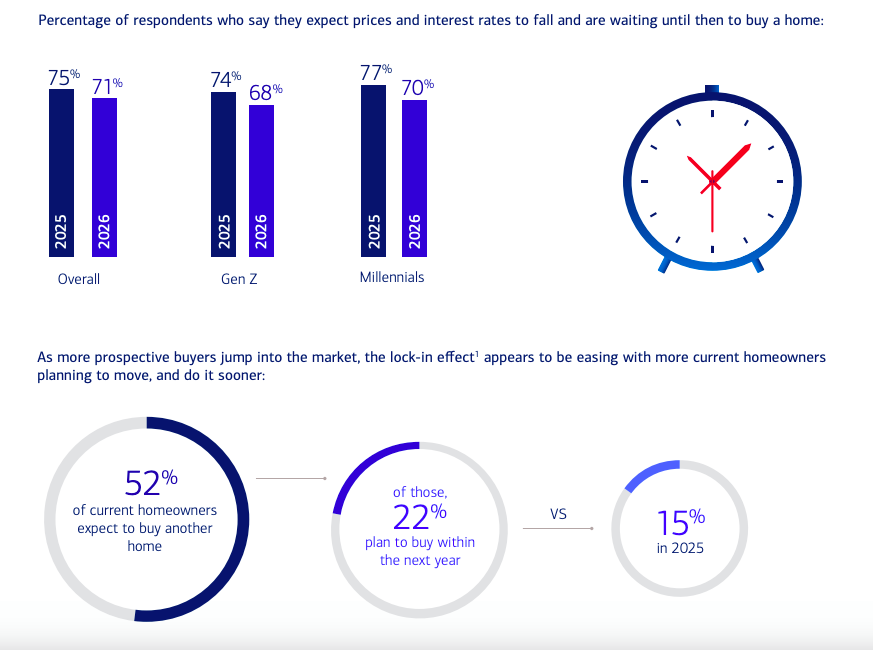

Bank of America’s 2026 Homebuyer Insights Report suggests consumer attitudes toward homeownership are becoming more optimistic even as mortgage rates and home prices remain elevated. For the first time since 2023, a majority of Americans (53%) say buying a home is a better option than renting or living with family. The report was based on a survey conducted between April 13 and May 10 of this year.

Affordability remains the biggest obstacle — with 58% citing high home prices as their biggest barrier to ownership and 47% pointing to mortgage rates — and some 71% of prospective buyers said they were delaying on making a home purchase until the situation improves. That’s four points lower than last year but still a lot of pent-up demand.

Matt Vernon, head of consumer lending for Bank of America, struck an optimistic tone in response to the numbers.

“We are seeing meaningful changes in attitudes toward homeownership,” he said. “Despite real and persistent challenges in the market, buyers and owners are increasingly optimistic, and many are starting to move forward rather than waiting on the sidelines.”

Q2 figures for the D-FW market will be available soon enough, which will give a picture of the war’s impact locally.

Zooming out, the latest U.S. Census Bureau report on new residential sales points to continued softness in the housing market. Sales of new single-family homes fell 7.3% in May, marking the second consecutive monthly decline and the slowest sales pace since January. Sales were also down 6.8% compared to May 2025, with the largest declines occurring in the South and West.