Seth Fowler: When it Comes to The Housing Market, Is 2022 The Next 2009?

Share News:

Remember the real estate world in 2009? Remember the Adjusted Rate Mortgages (ARMs) that most buyers were selecting as loan programs? Remember having plenty of home choices when looking for that right place? If you can remember that, then remember this … 2022 is not a replay of 2009.

While our Tarrant County Tuesday column has tried to impress that upon you lovely readers over the past few months, there are still people out there who either aren’t paying attention to my sage words of wisdom or they just want to believe what the national media is spewing regarding another housing bubble and crash and doom.

So take a deep breath and let’s get started.

In Case You Forgot

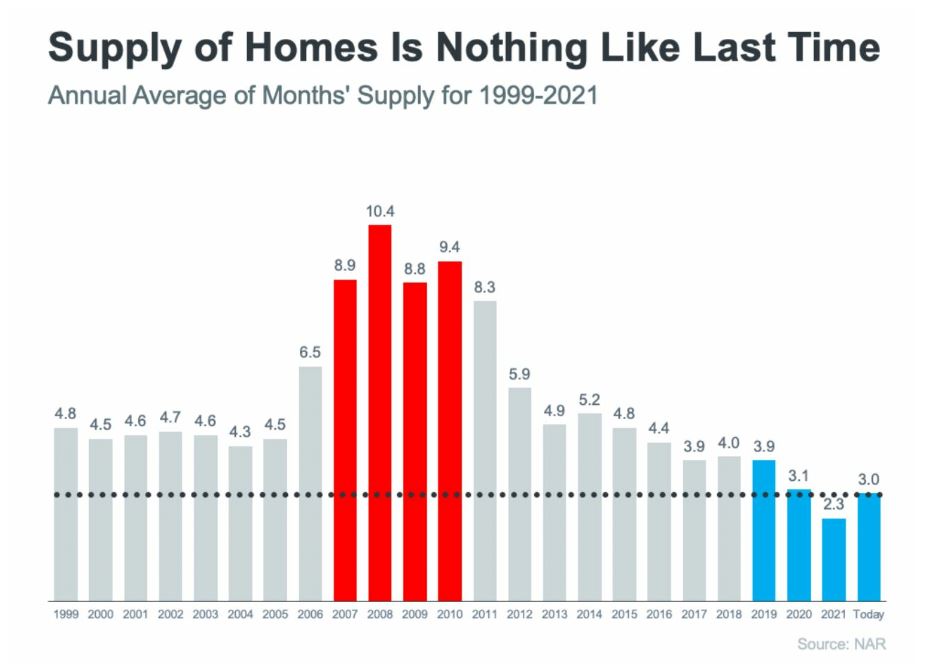

It’s okay if you need a refresher course. Sometimes I forget that “it’s all ball bearings nowadays.” Remember that a housing bubble is when there is rampant speculation in the housing industry so that prices are artificially high while inventory is also high. This was one of the key issues in the Great Recession of 2009. Inflated prices and plenty of homes to pick from.

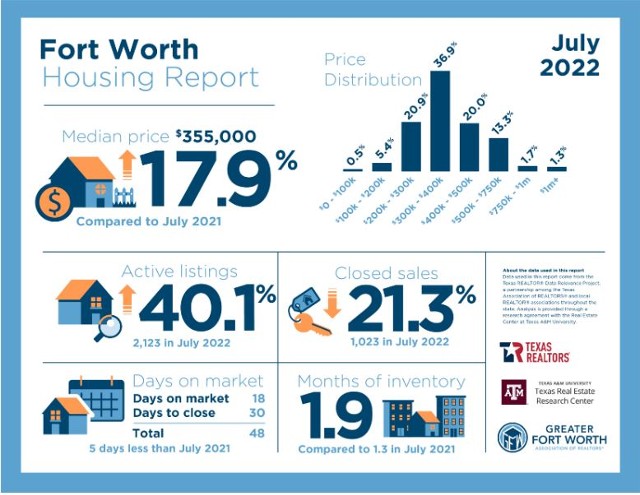

This is not at all like the real estate market in 2022 as we’ve discussed. Only recently has the monthly inventory of available homes exceeded one month. Remember, the monthly inventory is the number of homes closed in a particular area in a month divided by the number of homes available in that same area.

A balanced real estate market, where there is enough supply and demand, is said to be 6.6 months of inventory on the market. The July 2022 report has recently been released and the month’s supply is nearing two months.

There is still a tremendous lack of inventory in the Dallas-Fort Worth area. Prices are still high but inventory is still relatively low…therefore…we are not in a housing bubble.

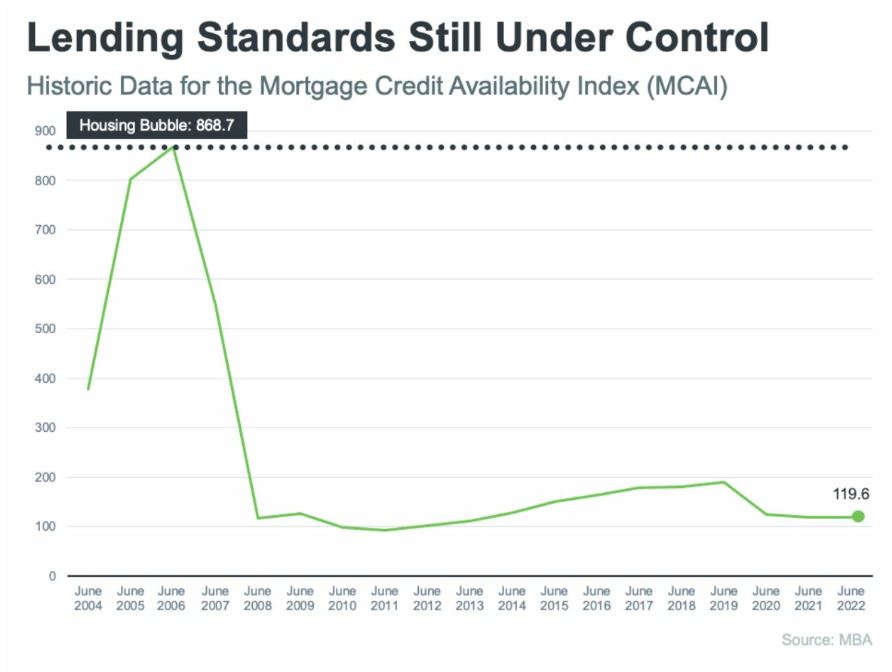

Everyone Gets A Loan … Even Dead People

I love my lender friends. They have those fancy calculators that I wasn’t allowed to have in high school, and they can talk all those numbers and things. It’s not their fault but dang, remember in 2009 when literally anyone could get a loan? Even dead people could be seen getting a loan.

The government and banks made it so much fun to buy a home back then. There were adjustable-rate mortgages (ARMs) where the buyer had a few years with an extremely low interest rate. Buyers could get a loan just by telling a lender what their income was and how much debt they had and not have to show any documentation or proof.

Getting a loan was like Oprah’s Christmas giveaway meme … everyone gets a loan! While that is fun for a few, when the ARM expired and the rate was going to adjust to the current day, homeowners had little equity in their homes and they weren’t able to pay the increased monthly payment. When the bill came due, many owners faced foreclosure.

Hopefully, banks, lenders, and the federal government have learned from their loosey-goosey lending criteria and will not make the same mistakes in 2022 that they did in 2009. Looking at the above image, we can already see that regulations and requirements for lenders are much tighter and not everyone gets a loan. Remember, if you can’t get a loan then you can’t buy a home.

Sorry to say but it looks as if the days of zero-doc loans and no income verification loans and all the other lending loopholes used by unscrupulous banks and lending companies are not going to be making a comeback anytime soon.

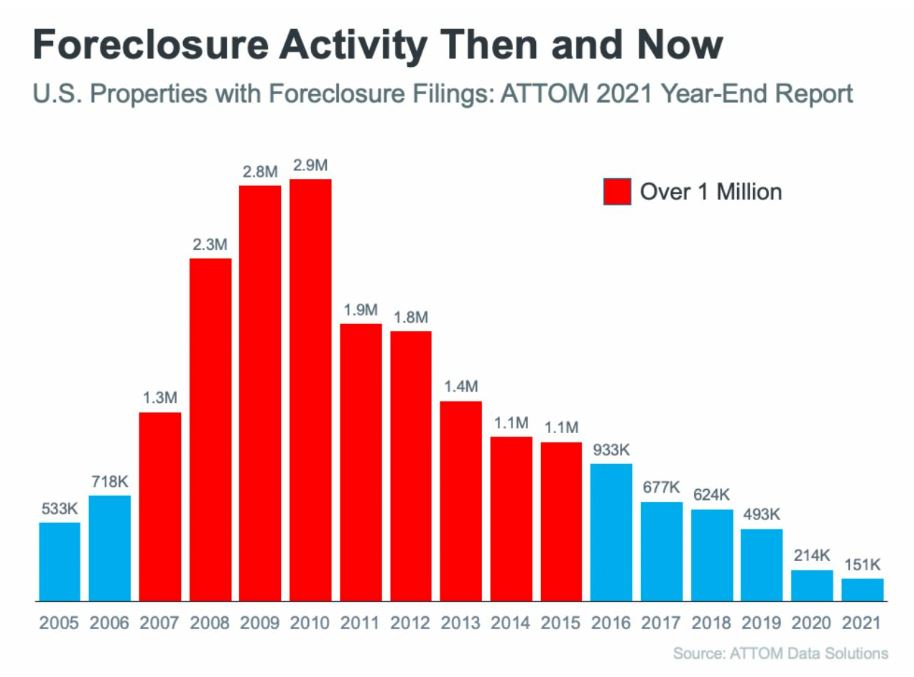

Homes on The Auction Block

Foreclosure — whew did we have a ton of foreclosures during the Great Recession. When homeowners couldn’t afford the home, there was no equity (value) in the home, and no market in which to sell their home, they simply walked away and let the banks repossess the property.

The stories across the country were horrifying. Images of abandoned homes and entire neighborhoods were appalling to see. It was tragic and heartbreaking.

Repeat after me: “We are not, not, not going to have foreclosure issues as we did in the past.”

Remember that and don’t forget it.

Why is it so different in 2022 than in 2009? First of all, that COVID-19 thing happened and the government forbid any foreclosures from happening in 2021. Secondly, because of the increasing value of homes, even if an owner couldn’t make their monthly payments, they could still put their home on the market, sell it, and use the equity to pay off their note. They might even have some money left over.

Yes, but …

Yes, the real estate market is cooling off from the past 24 months. Yes, interest rates are a factor. Yes, inflation isn’t helping either.

But, this is not the beginning of the end of the world. Because of very tangible things such as stricter lending requirements, continued low inventory of available homes, and built-up equity in homes over the past few years, we are not going to see a total collapse of the real estate market.

Do prices of existing and new construction homes need to drop? Absolutely! Reluctantly sellers are starting to listen to their real estate sales professionals and reducing the asking price for their homes. While it might take a while longer, eventually new construction homes will be reduced enough to move inventory.

The sooner everyone involved gets on board and understands that a balancing market is a good thing for the entire economy, the better. Landowners need to come down on their asking prices. Laborers need to take a little less. The cost of goods and building materials need to go back to realistic prices (although days of pre-COVID pricing I’m afraid are gone). Builders need to not keep passing all their price hikes to the consumer. The sooner new homes are once again affordable to first-time home buyers the sooner the housing market will get back on track.

But Don’t Expect it Tomorrow

Will it take a while? Yes. How long is a while? No one knows. It appears the interest rate is stabilizing and gas prices are as well. As the fall rolls around and people come home from vacation and realize the world is not ending and economies aren’t collapsing, they will start looking to buy and sell once again.

Remember: 2022 is not a repeat of 2009. Now go and remind everyone you know.

Hi Seth,

Along with banks, lenders, and the federal government, following 2009, realtors also learned to not encourage clients to purchase homes priced beyond their budget limitations.

On another matter, why is your bubble in photo #1 floating above the Pacific Heights neighborhood of San Francisco, instead of the Park Cities? Is it because the San Francisco Bay Area real estate market is also diminishing, with lower prices and lower sales?

Hedda

Ha…not sure if San Francisco or any California will ever be associated with “lower prices” or anything…you have to talk to my editor about photo choice – not the one I had inserted…but I just type the words and stay in my lane. Thanks for reading and following and commenting…let’s hope many people learned (and remember!) the pitfalls, greed and idiocracy of 2009

Ha! Way to throw your editor under the bus!

The choice on the lead image was made because it filled the space and had more visual impact.