Census Bureau

Tis the season for bell-ringing kettle drives, helping needy families, and giving to homeless shelters. But there’s one city in North Texas that keeps this lovely Christmas spirit all year long. It’s Plano. The North Texas city recently earned a top spot in the rankings as one of the most caring cities in America, according…

According to Census estimates, Texas added 537,000 to 582,000 incoming residents in 2019. The Census estimated outgoing residents numbering between 435,000 to 471,000, yielding the 100K net gain. Texas also gained 192K to 220K residents from outside the U.S. in 2019.

Collin County neighbors Frisco and McKinney ranked 1-2 in RentCafé’s latest report on top-20 suburbs with most new apartments in the past five years.

The projection of Californians migrating en masse to Texas for job opportunities and lower taxes in 2020 wasn’t quite as drastic as first believed, according to U.S. Census Bureau data. In 2018, a Texas Realtors Association report showing Californians were migrating to Texas at a more than 2-to-1 rate showed no reason to think it…

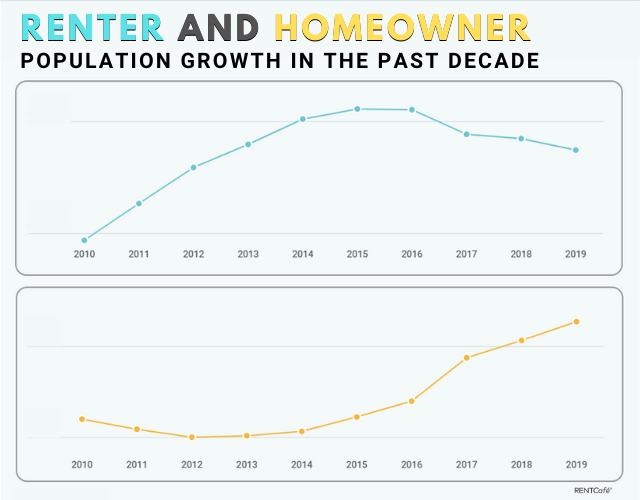

Out of 314 U.S. cities, Frisco and Plano ranked first and second in a new study that tracked the increase in the percentage of renters vs. homeowners over the past decade. Yes, that’s correct: Frisco and Plano lead the nation in residents choosing to rent an apartment versus buying a condo or home. Frisco more…