Housing Affordability Continues to Decline in North Texas as First-Time Buyers Dwindle

Share News:

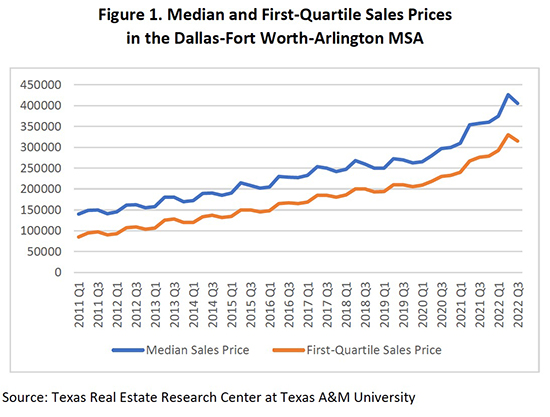

It seems cruel that, just when listings are posting “price improvements” and the number of days on market are inching upward, interest rates are making what was once buying power for a $400,000 home barely enough to snatch up something in the $300s. According to the most recent housing affordability report from the Texas Real Estate Research Center, home prices are continuing to outstrip income growth while interest rates further constrict home purchasing potential.

Housing Affordability And The Income Gap

The report, which covers the Dallas-Fort Worth-Arlington MSA, shows that the median home price for the region is up 13.3 percent year-over-year while median family income has only increased by 9.4 percent.

“The growth in the gap between median home price and family income has been fueled by significant home price appreciation (particularly during the initial stages of the COVID-19 pandemic) and relatively sluggish growth in incomes,” says Dr. Clare Losey, assistant research economist at the Texas Real Estate Research Center. “To close the gap, either home prices must decrease, or family income must increase (or both).”

However, the gap between home price and income only tells one part of the story, Losey said. Another is, of course, the rise in mortgage rates. Rates averaged 5.62 percent in the third quarter of 2022, up considerably from the first quarter (3.82 percent) and slightly from the second quarter (5.27 percent). And while the median home price grew only 13.3 percent year-over-year compared to 20.4 percent in 2021, inflation will mean that housing affordability will hinge on whether a potential buyer can keep up with payments at all.

“We’re already starting to see a moderation in home price appreciation. With inflation, households’ purchasing power diminishes — in other words, households spend a higher proportion of their income on basic goods and services,” Losey said. “Although inflation doesn’t affect the household’s ability to qualify for a mortgage loan per se (the required income to qualify is a function of the applicant’s income, wealth, and credit), it could make it more difficult for the buyer to maintain timely monthly mortgage payments if inflation sufficiently diminishes the funds for other necessities, like food, transportation, and medical care.”

First-Time Buyers Are Older, Fewer, And Plan to Stay Longer

The report from TRERC comes at the same time the National Association of Realtors released its 2022 Profile of Buyers and Sellers. The report shows that first-time buyers are fewer and older than ever before.

NAR’s data shows that first-time buyers made up only 26 percent of the market, down from 34 percent last year and a peak of 50 percent in 2010 during the First-Time Home Buyer Tax Credit. Plus, the age of the average first-time buyer was 36 years — up from 33 in 2021.

“It’s not surprising that the share of first-time buyers shrank to the lowest level ever recorded given the housing market’s combination of historically low inventory, persistently high home prices, and rapidly escalating interest rates,” said Jessica Lautz, NAR vice president of demographics and behavioral insights. “Those who have housing equity hold the cards and they’ve fared very well in the current real estate market. First-time buyers are older as a result of saving for down payments for longer periods of time or relying on a generational transfer of wealth to propel them into homeownership.”

According to the report, not only are these first-time buyers older and rarer, but they’ll likely live in the same home longer as their expected tenure is 18 years, up from just a decade last year.

“Given the significant headwinds facing potential buyers — still-elevated home prices, higher mortgage rates, and still-constrained supply (i.e., inventory for sale), it’s of no surprise that 1) first-time buyers comprise a smaller proportion of buyers overall and 2) the average age of buyers is trending older,” Losey said. “With respect to the first point, first-time buyers tend to be younger and of lower income. In other words, these buyers have not matriculated through the labor force and therefore achieved peak earnings. Income, wealth, and credit all tend to pose a constraint for first-time buyers, and with still-elevated home prices, first-time buyers are going to particularly struggle in overcoming the wealth barrier (i.e., making the down payment). Meanwhile, still-elevated home prices and higher rates raise the income required to qualify for a mortgage loan. With respect to the second point, ‘older’ buyers tend to have higher savings and to be of higher income. This simply makes qualifying for a mortgage loan much easier, and therefore homeownership is more accessible to them.”