Is it a Buyer’s Market? Home Sales Are Down And Inventory is up, But Interest Rates Aren’t Helping

Share News:

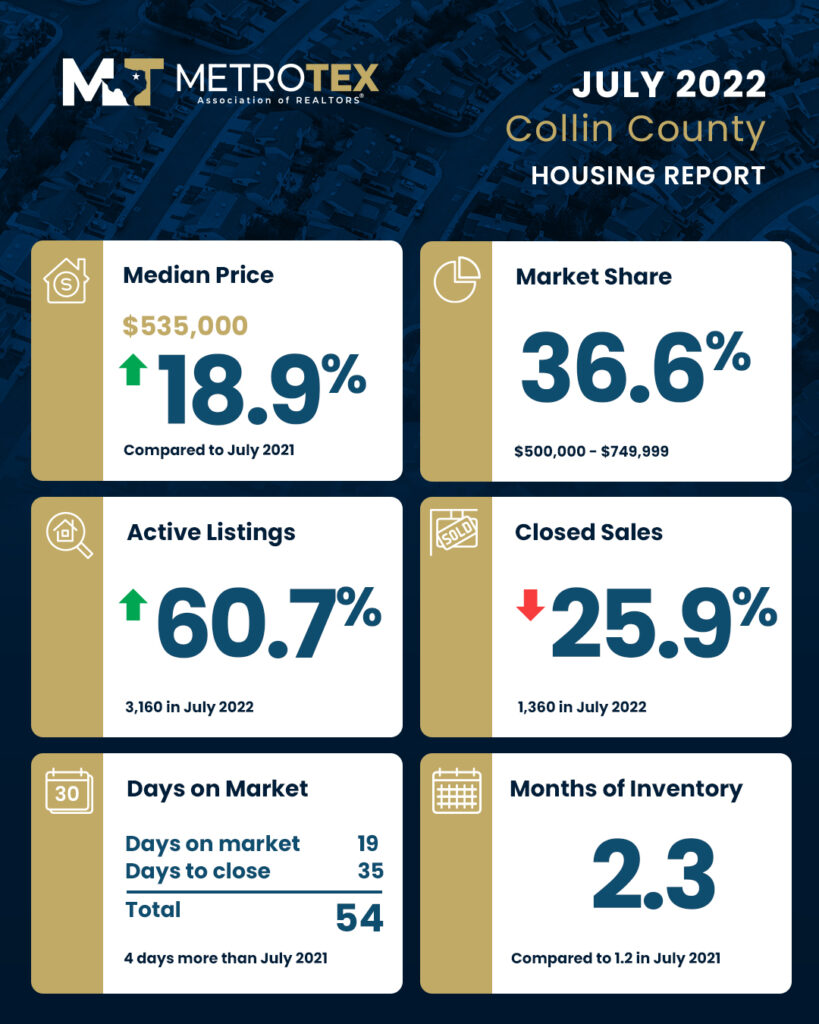

The National Association of Realtors just released a report showing existing home sales sliding by 5.9 percent in July from the previous month. That’s the sixth month in a row of declining sales numbers. Statewide statistics reflect a cooling market, too, with closed sales down 16.1 percent for July according to recently released numbers from MetroTex Assocation of Realtors.

More Homes, Fewer Sales

As sales numbers have declined, inventory has increased.

Nationally, inventory of unsold existing homes increased to 1.31 million in July, which is the equivalent of 3.3 months of inventory at the current pace. In Texas, inventory has increased by almost a full month of available housing to 2.5 months of inventory at the current sales pace. A balanced market, according to the Texas Real Estate Research Center, is approximately 6.5 months of inventory.

So with declining sales and more homes on the market, it should be easier for buyers to snag their dream house, right? Not so much, says NAR Chief Economist Lawrence Yun.

“The ongoing sales decline reflects the impact of the mortgage rate peak of 6 percent in early June,” Yun said. “Home sales may soon stabilize since mortgage rates have fallen to near 5 percent, thereby giving an additional boost of purchasing power to home buyers.”

“Price Improvement”

It’s true that the Dallas-Fort Worth region has seen a trend toward “price improvements,” with 3,824 listings posting price reductions in the past seven days. But interest rates hovering around 5 percent are keeping some buyers out of the market. That’s a far cry from the 3.6 percent to 3.9 percent rates in the months before the pandemic.

“We’re witnessing a housing recession in terms of declining home sales and home building,” Yun added. “However, it’s not a recession in home prices. Inventory remains tight and prices continue to rise nationally with nearly 40 percent of homes still commanding the full list price.”

The number of days a home is on the market is another indicator. Fewer days on market means a higher level of demand. MetroTex’s most recent figures show that listings remain on MLS for an average of 19 days in Dallas, Denton, and Collin counties. In Tarrant County, listings linger on the market for just 17 days. For the most part, that’s fewer days on market than July 2021, with the exception of Denton County, which has increased days on market by just one.

Watching Jobs, With Interest

So if the market’s not balanced, days on market are still trim, and interest rates aren’t helping buyers catch a deal, what about the recent jobs report? Well, there’s good news and bad news.

“July saw a solid jobs number, with 528,000 net new payroll additions. The 20 million jobs lost during the early months of the COVID-19 lockdown have been fully recovered,” Yun said in a statement. “More Americans are working today than at any time in history. The unemployment rate is 3.5 percent, matching a 50-year low.”

While that’s great, wages have only increased by 6.2 percent according to the most recent report from the U.S. Bureau of Labor Statistics. That’s not enough to keep up with the 9 percent rate of inflation, though wage increases could be in the pipeline. And again, the lack of enticing mortgage rates isn’t helping.

“In other words, home sales are more impacted by mortgage rate changes than jobs,” Yun explained. “But the recently stabilizing mortgage rates suggest home sales will also soon stabilize and are likely to make steady gains in 2023.”