Jonathan Miller

by Jonathan Miller Special Contributor I made the trek to Bed Bath & Beyond with family in tow many times until its demise in 2023. It was a national big‑box retailer, the anchor of many shopping malls in my local area, with nearly 1,600 stores nationwide. The chain specialized in housewares, furniture, and seemingly random gadgets…

By Jonathan MillerSpecial Contributor Takeaways Thinking About Real Estate as a Bank Safety Deposit Box There’s a lot here to consider for a Friday afternoon and the first day of spring, but hey, you’ve got all weekend, and the test isn’t until Monday. Investors are always searching for assets that don’t move in the same…

By Jonathan MillerSpecial Contributor Understanding Housing Market Trends ASAP Admittedly, going into the Beige Book and anecdotal is a little wonky, but I promise it is worth it. Here it goes… Everyone who interacts with the housing market has all heard this debate between pending and closed sales: Early on, brokerage firms that tried to…

By Jonathan MillerSpecial Contributor 2026 Looks To Be A More Active Year For The Housing Market Inflation, which housing accounts for a third of its calculation, has been a consistent topic throughout the year, as shown in this incredible AXIOS visualization. Mortgage rates are expected to fall a little next year, while markets are betting the Fed will…

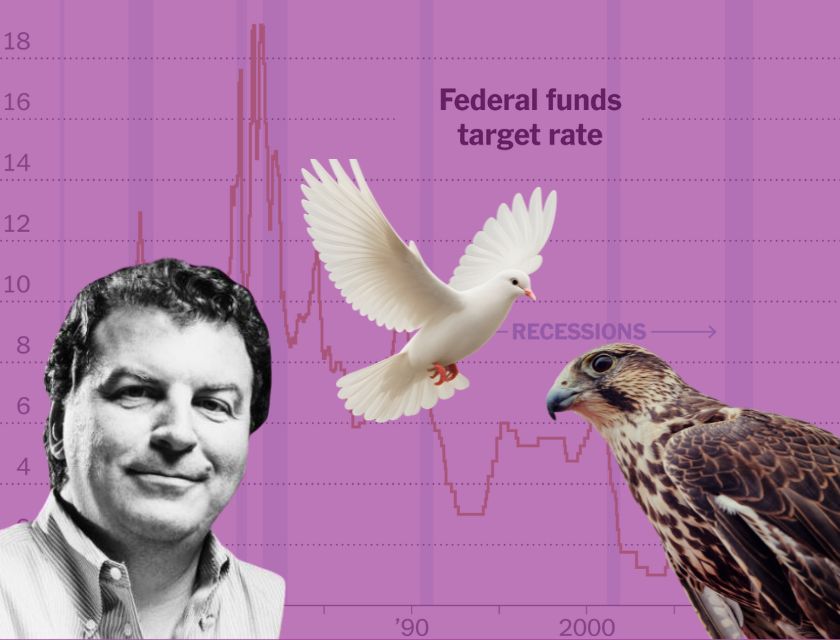

By Jonathan MillerSpecial Contributor The Fed Cuts And The Search For A Heart Of Gold Neil Young’s 1980 political album Hawks & Doves was disappointing to his fans after the barn-burner Rust Never Sleeps and the classics After the Gold Rush and Harvest set the standard. For me, the Hawks & Doves album symbolized the beginning of a weaker era of his albums and perhaps,…