Getting Real About Renos: Will New Insulation Really Add Value to My Home?

Share News:

Photo: Moppet via Creative Commons

This is the third installment of a new occasional column called Getting Real About Renovations. We’re looking at renovation realities for all sorts of projects, from hardwood floors and open floorplans, to master suite additions and kitchen upgrades. We’ll give you the unadulterated truth about options, costs, effort, Realtor opinion, and estimated ROI for these projects. You can read the last one about garage doors here.

When people think of home renovations, things like “new kitchen” and “hardwood floors” typically come to mind. But when it comes to bang for your buck — and it might not be as sexy as a new vaulted ceiling or bathroom tile treatment — you really can’t beat adding insulation.

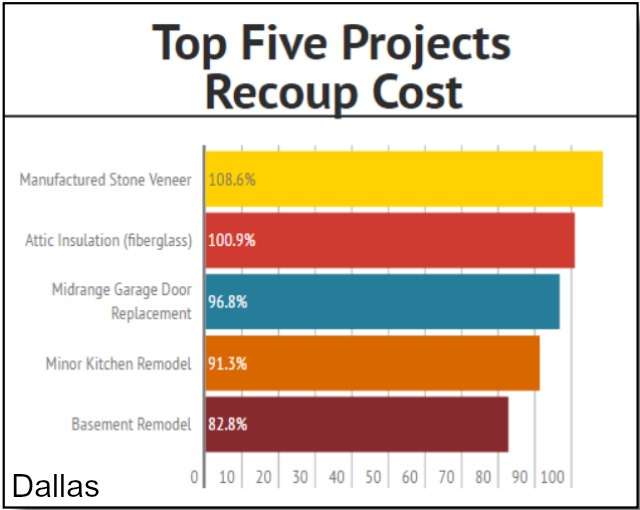

Both nationally and in Dallas, the top home remodeling projects last year were those that increased the functionality and sustainability of the home. They did this by improving either a home’s drive-up appeal or energy efficiency, according to the 2016 Cost vs. Value Report by the National Association of Realtors and Remodeling magazine.

Fiberglass attic insulation, which increases a home’s energy efficiency, ranked among the top five most profitable projects nationwide. In Dallas, it recouped 100.9 percent of initial investment, based on an average project cost of $1,482, according to that report.

“I think adding insulation is a great ROI in most cases —it is relatively inexpensive, as compared with radiant barrier, HVAC, solar panels, and a lot of other energy efficiency features,” said Kay Wood, a Realtor with Briggs Freeman Sotheby’s International Realty. “There are also sometimes incentives from Oncor or federal tax credits for increasing the efficiency of your home. I always encourage clients to think about how long they plan to stay in their home and how long it looks like it will take to see that savings pay for their investment. Energy efficiency and green features can also improve resale.”

Source: 2016 Cost vs. Value Report by the National Association of Realtors and Remodeling magazine

Another recent report, the 2015 Remodeling Impact Report from the National Association of Realtors and National Association of the Remodeling Industry, estimates a 95 percent return on investment for insulation upgrades, with an average project cost of $2,050. It does not clarify the specific type of insulation.

Here’s their breakdown of the metrics on consumers’ viewpoint after completing the project:

- Top reason for doing the project: to improve energy efficiency (71 percent)

- Most important result: better energy efficiency (30 percent)

- About 61 percent of homeowners have a greater desire to be home since completing the project, and 61 percent have a major sense of accomplishment when they think of the project

- Joy score: 8.7 out of 10

“At my last home, I used an Oncor subsidy and a tax credit to help pay for insulation and radiant barrier at my 1930s cottage,” said Wood. “The energy savings, along with the incentives, paid for the whole thing in less than three years, and after that, we just got to enjoy the lower bills and more comfortable house in the summer!”

Realtor Alison Houpt-Howell, also with Briggs Freeman Sotheby’s International Realty, agreed, saying attic insulation is a low-cost investment that can save a homeowner hundreds, if not thousands, in terms of the length of time they plan on spending at their current residence.

“From today’s discerning buyer’s standpoint, knowing that you can purchase an older home full of character that also has energy-efficient features is a win-win in today’s competitive market,” Houpt-Howell said. “I cannot see any reason why someone would not consider adding attic insulation to their home.”

Michael Reynolds, a Realtor with UResidential, had some closing thoughts:

“Adding insulation is one of the most cost effective ways to increase value on my clients’ homes,” Reynolds said. “Not to mention, new insulation assists in helping with the rising cost of electricity, which is huge for homeowners.”

To bring this topic into the real world, it is critical to address the root cause of the chasm between what scientific studies of what buyers indicate that they are willing to pay a premium amount for a home and what a seller actually experiences with an agent and then subsequently with an appraiser, assuming that the buyer requires a mortgage.

The root cause of this problem is that those who

determine policy in residential finance and valuation have not required specific data fields, and thus information gathering by agents and by appraisers to quantify and thus monetize the value added by these energy enhancements.

We made significant energy efficiency enhancements to a custom home purchased new in Dallas in 1979 which we fully intended to live in forever.

It was noteworthy that in a cash-out refinancing to fund remodeling expenditures with the

purchase money mortgager, one Wells Fargo Bank, their appraiser put zero value added on the

significant expenditures that had been made that

resulted in our summer electric bills being one half that of our neighbors, who had comparable square footage.

The appraiser’s exact comments were: “Ah, the banks don’t care about that stuff.”

Separarately, if you add blown in fiberglass added to that which has flattened out in your attic, be sure to have cylinders placed above your soffit vents, or you will block the essential ventilation through your attic.

While it is outside the scope of this piece, there is

exactly the same problem with a failure to capture data which would lead to the recognition of value added to a home by professional landscape architecture implementation.

To state clearly the status quo, if you do not get your lender or your Realtor to agree in writing that the value added by your energy efficiency enhancements, as well as your professional landscape architecture implementation, you may well see no return on those significant investments, which informed buyers seek.

To encourage this becoming a reality during my lifetime in the sluggish residential market, I will forward a copy ofor this comment to the Executive Office of the holding company that owns the cited Wells Fargo Bank.

The appraiser’s exact comments were: “Ah, the banks don’t care about that stuff.”

——–

I think there is some distinction between a refi vs a new buyer. The bank can’t take insulation upgrades into account because the same result could be achieved (less monthly cash outlay) by simply turning up the thermostat in summer. The bank doesn’t care if you are comfortable.

The next buyer does, especially in a climate like TX, and if you can show a comfortable house with copies of your past summertime bills, a rational buyer will take that into account.

While the Overdog’s comment may well be accurate, doing things the way that they have always been done

is a recipe for failure in a competitive environment.

The moment that a well managed competitor in the residential financing field determines that it will implement proper information technology protocols to properly identify those properties that are the most attractive ( and thus easier to sell if they become owned by the bank as foreclosed collateral ) and probably held by the most desirable customers, it will eat the lunch of its more lethargic competitors who tolerate sloppy appraisal protocols.

This is one way to mitigate the immense problem of the disadvantage faced by those who must secure a mortgage in a very competitive seller’s market which has far more buyers than attractive properties. Many of these buyers have just sold homes in very expensive housing markets and have upper six figures in their bank accounts from the tax free capital gain on the sale of their prior residence.

A seller faces a great deal of uncertainty from the professionalism and willingness to perform of the appraiser and it is common to have an appraisal that is far less than multiple cash offers for the same property with a relevant time frame.

Any asset is worth what a willing buyer under no duress is willing to pay for it given adequate information.

The actual process in effect in Dallas results in an understatement of the value of homes in this rapidly escalating home value environment driven by professional job growth, not speculation.

The mortgage lender that adapts its processes to attract the most desirable customers will thrive; those who cling to outmoded methods will end up with the slow pay and less desirable customers and thus be assured of experiencing higher loan losses than its more effectively managed and innovative competitors, who will have lower loan losses.

Financing homes is a numbers game – as in large numbers smooth out differences between homes, and ‘information’ about each individual home really has no effect compared to ‘information’ about the local economic climate. Especially in a ‘stateless’ area like Dallas, where entire cities are essentially interchangeable based on highway commute – DFW is not the place where the Italians all live in the same neighborhood for example and have for 100 years….

If sales slow such that cataloguing the minute differences between each home matters, then such a plan will be executed.